Retirement is a journey, not a single event. This roadmap breaks retirement into six stages — from early accumulation to late-life legacy planning — and provides focused goals, common risks, practical priorities and immediate “If you are here — do this now” actions for each stage. Use the Table of Contents to jump to any section, and follow the cross-stage checklist to keep your plan current.

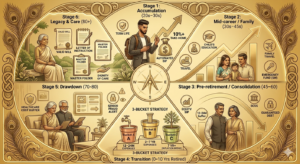

Stage 1 — Accumulation (20s–30s)

Goal: Build saving habits, emergency fund and tax-efficient long-term growth.

Common risks

- Procrastination, low savings rate

- High discretionary spending

- Inadequate insurance

What to prioritise

- Emergency fund: 3–6 months of essential expenses (more if freelancing)

- Automated SIPs into equity mutual funds / ETFs (large-cap, multi-cap)

- Use tax-efficient instruments (PF/PPF/NPS where applicable)

- Buy term life insurance if you have dependants; basic family health cover

- Avoid high-interest unsecured debt; pay credit cards monthly

If you are here — do this now

- Automate a SIP equal to at least 10% of take-home pay

- Open PPF and/or start NPS if employer pension is inadequate

- Buy term life cover (if family depends on your income) and a basic health policy

Stage 2 — Mid‑career / Family Building (30s–45s)

Goal: Grow corpus quickly while securing family and education goals.

Common risks

- Lifestyle inflation

- Over-concentration in property

- Emotional lending to family; inadequate contingency for children’s needs

What to prioritise

- Increase equity allocation (SIPs) and diversify across fund types

- Top‑up PPF and consider VPF for higher fixed contributions

- Create dedicated goal funds (children’s education, house repairs)

- Increase term cover and health insurance limits; consider critical illness riders

- Prioritise repayment of high-rate debt; build 6–12 months contingency fund

If you are here — do this now

- Project child education and marriage costs and begin dedicated SIPs

- Cap unsecured loans to a safe percentage of net income and plan aggressive repayment

- Formalise any financial help to relatives with documented loans/gifts

Stage 3 — Pre‑retirement / Consolidation (45–60)

Goal: Protect capital, reduce volatility, estimate retirement corpus and plan tax-efficient decumulation.

Common risks

- Late catch-up investing with high equity exposure

- Underestimating life and healthcare costs

What to prioritise

- Recalculate retirement needs with conservative inflation and withdrawal assumptions (e.g., 3–4% WR)

- Adopt a glidepath: gradually reduce risk but retain equity for growth

- Maximise retirement accounts (EPF/VPF/PPF/NPS contributions)

- Build a health corpus and upgrade family health/critical illness cover

- Reduce large debts, especially unsecured or high-rate long-term loans

If you are here — do this now

- Run a gap analysis: projected corpus vs required corpus; increase SIPs or adjust mix if needed

- Set aside a 12–24 month liquid buffer before retirement

- Speak with a certified financial planner for annuity vs lump-sum tradeoffs and tax planning

Stage 4 — Transition to Retirement (first 0–10 years after retirement)

Goal: Build a safe income plan and avoid sequence‑of‑returns risk.

Common risks

- Panic selling amid market downturns

- Emotional overspending for family events

- Relying on uncertain family support

What to prioritise

- Implement a bucket strategy: Bucket A (0–2 yrs liquid), B (2–7 yrs bonds/liquid), C (>7 yrs equity)

- Lock guaranteed income for basic expenses (part annuity, SCSS, pension)

- Rebalance for lower volatility but keep an equity cushion for inflation protection

- Plan tax-efficient withdrawal sequencing across account types

If you are here — do this now

- Build Bucket A = 12–24 months of expenses in liquid vehicles

- Decide on an annuity or guaranteed product for essential expenses

- Document withdrawal rules (monthly/yearly) and avoid ad hoc large gifts from the corpus

Stage 5 — Established Retirement / Drawdown (70–80)

Goal: Maintain lifestyle, preserve capital and meet healthcare needs.

Common risks

- Rising healthcare and long-term care costs

- Cognitive decline affecting financial decisions

- Scams targeting seniors

What to prioritise

- Keep short-term needs in safe instruments (SCSS, short-term bonds, FDs, liquid funds)

- Maintain a measured equity exposure for inflation hedge (10–20% depending on tolerance)

- Regularly review annuity/pension payments and tax impact

- Reinforce fraud prevention and arrange trusted assistance for banking

If you are here — do this now

- Review and top-up senior health policies

- Consolidate accounts, update nominees and authorize trusted helpers for routine tasks

- Plan for in-home care or assisted living options and factor costs into the budget

Stage 6 — Late Retirement / Legacy & Care (80+)

Goal: Ensure dignity of care, simplify estate settlement and pass a clear legacy.

Common risks

- Frailty and cognitive impairment

- Confused legal succession and last-minute disputes

What to prioritise

- Simplify finances: fewer accounts, clear nominees and an accessible will

- Keep records of loans, gifts and intentions to avoid disputes

- Plan long-term care funding (medical, home help, hospice) and consider selling or renting unused property

- Make legacy wishes explicit (charitable bequests, distribution of heirlooms, funeral wishes)

If you are here — do this now

- Update or revalidate the will; prepare a Letter of Instruction for heirs

- Keep all important documents (ID, property deeds, insurance) together and accessible

- Discuss wishes openly with executor and immediate family to reduce conflict

Sample glidepath (illustrative)

Use this as a guide — tailor to your risk tolerance and goals.

- Early career: Equity 80%, Debt 10%, Cash 10%

- Mid‑career: Equity 65–75%, Debt 15–25%, Cash 5–10%

- Pre‑retirement: Equity 40–60%, Debt 30–45%, Cash 5–15%

- Transition/Retired: Equity 15–35%, Debt/Guaranteed 50–70%, Cash 15–25%

- Late retirement: Equity 10–20%, Debt/Guaranteed 60–75%, Cash 15–25%

Cross‑Stage Checklist & Practical Tools

Annual actions

- Rebalance portfolio and update net worth statement

- Check and update nominees and beneficiary details

- Review health cover and top-ups

On major life events (marriage, child, home sale)

- Revisit allocation, insurance and will

- Document new loans/gifts and update family rules

Ongoing

- Automate savings and SIPs

- Maintain emergency fund and liquidity for the next life stage

- Avoid emotional over-support of adult children at your expense

Practical tools to consider

- Government/public schemes (EPF, PPF, NPS, SCSS, PMVVY as applicable)

- Tax planning: use pre-retirement tax benefits (80C, 80CCD etc.) and consult a tax expert

- Estate planning: updated will, nominations, and a one‑page Access Card with key contacts