Retirement planning in India is not one-size-fits-all. Couples benefit from shared expenses, while singles bear the full burden of costs. With rising longevity and high medical inflation, calculating the right retirement corpus is critical for a stress-free second innings.

This guide breaks down the key differences, provides a step-by-step calculation method, real examples, and actionable tips for both couples and singles.

Why Corpus Needs Differ for Couples vs Singles

Two people living together don’t need double the corpus of one person. Shared households enjoy economies of scale, but they also face unique risks around longevity and survivorship.

| Financial Factor | Impact on Singles | Impact on Couples (Joint Planning) |

|---|---|---|

| Economies of Scale | Bears 100% of housing, utilities, and domestic help | Shared costs significantly reduce per-person expense |

| Longevity Risk | Plan for one lifespan | Must plan for longer joint horizon + surviving spouse |

| Healthcare Inflation | Medical needs for one person | Higher chance one spouse needs long-term care |

| Guaranteed Incomes | Single pension / benefits | Complex family pension & survivor benefits (EPS, etc.) |

Step-by-Step Guide: How to Calculate Your Retirement Corpus

Core Formula

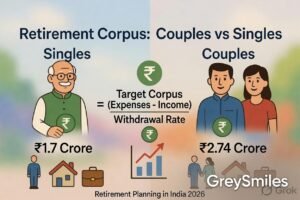

Target Corpus = (Annual Net Expenses - Guaranteed Income) / Safe Withdrawal Rate

- Estimate Annual Net Spending – Create a realistic retirement budget (monthly × 12). For couples, prepare a joint budget including housing, groceries, travel, and healthcare.

- Adjust for Inflation – Use 6% general inflation and 8–10% for medical inflation in India.

- Subtract Guaranteed Incomes – EPF pension, EPS, NPS annuity, rental income, SCSS, family pension, etc.

- Choose Safe Withdrawal Rate

Singles: 3.5% – 4%

Couples: 3% – 3.5% (due to longer combined lifespan) - Apply the Formula to get your target corpus.

Practical Examples (2026 Context)

Example 1: Single Retiree (Bengaluru)

- Annual expenses: ₹8,00,000

- Guaranteed income: ₹1,20,000

- Net expenses: ₹6,80,000

- Withdrawal rate: 4%

- Required Corpus: ₹1.70 Crore

Example 2: Couple (Pune)

- Combined annual expenses: ₹12,00,000

- Guaranteed income: ₹2,40,000

- Net expenses: ₹9,60,000

- Withdrawal rate: 3.5%

- Required Corpus: ₹2.74 Crore

Note: The couple’s corpus is significantly less than double the single’s due to shared living costs.

Practical Joint Planning Steps for Indian Families

- Create a Transition Budget and forecast post-retirement changes.

- Map Survivorship Benefits (family pension, EPS, insurance).

- Secure strong family floater + super top-up health insurance.

- Optimize tax-efficient withdrawals.

- Use the 3-Bucket Strategy for risk management.

- Formalize Estate Planning (Will, nominations, joint access).

- Review the plan every 1–2 years.

Special Considerations & Risks

- Medical Inflation – Often 8–12% annually. Build a dedicated healthcare corpus.

- Sequence of Returns Risk – Protect early retirement years with conservative buckets.

- One-Earner Households – Ensure both partners have financial visibility and literacy.

- Real Estate – A debt-free home significantly lowers required corpus.

Quick Checklist Before Finalizing Your Corpus

- Realistic joint or individual budget prepared?

- Medical inflation and long-term care factored in?

- All pensions and survivor benefits documented?

- Portfolio stress-tested at 3–4% withdrawal rate?

- Both partners have full financial visibility?

Conclusion

Whether you are planning as a couple or single, a thoughtful retirement corpus calculation gives you clarity and confidence. The goal is not just to survive retirement — but to enjoy a meaningful and financially secure second innings.