Start executing your retirement planning for salaried employees in india today to secure a calm, financially independent life later. This comprehensive guide helps corporate and salaried individuals estimate their required post-career corpus accurately. Furthermore, it outlines how to optimize long-term wealth-building tools like EPF, NPS, PPF, and mutual fund SIPs. You will also learn to protect your hard-earned savings using robust insurance strategies and emergency funds. Ultimately, mastering your asset allocation eliminates guesswork, letting you transition into your golden years with absolute confidence.

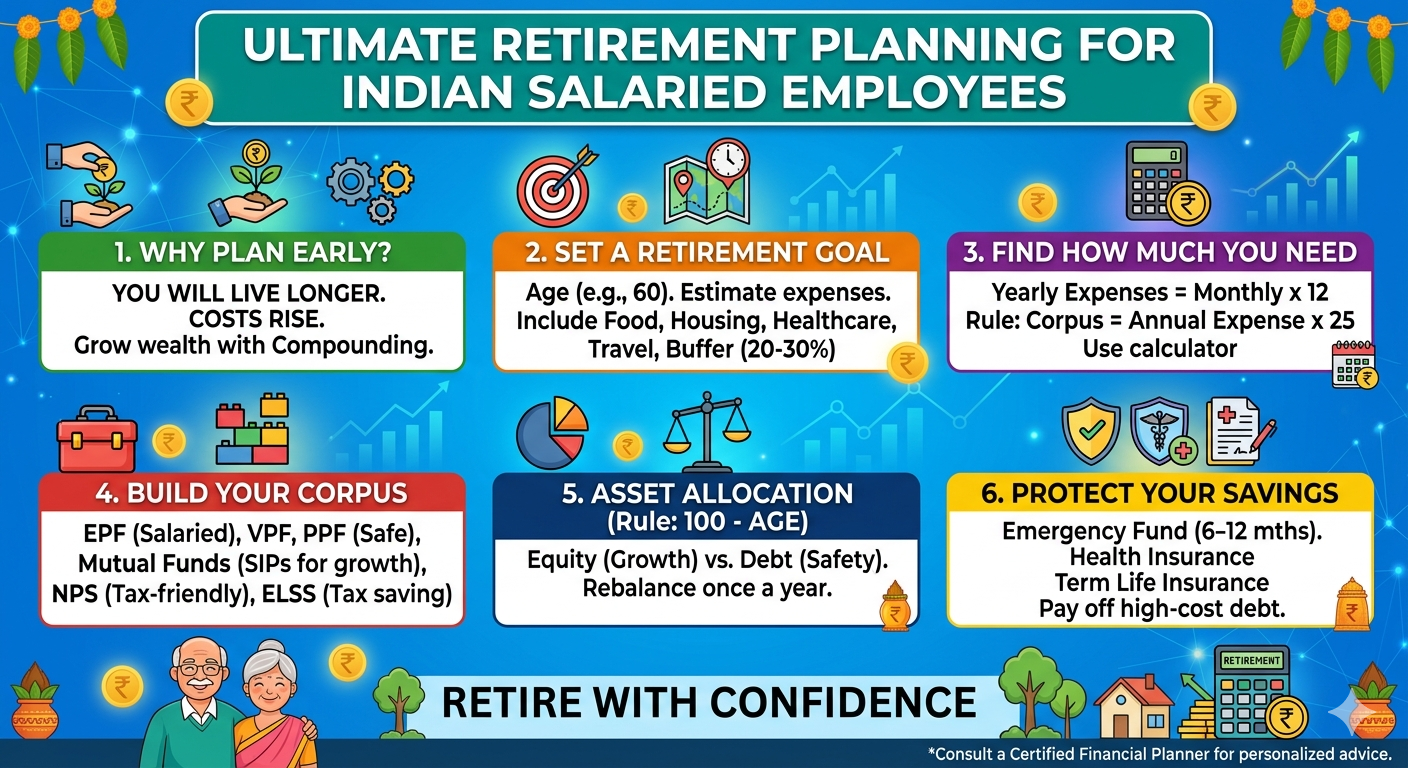

Why You Must Plan for Retirement Early

- The Longevity Reality: Average life expectancies are rising consistently across the subcontinent. Consequently, your accumulated corpus needs to sustain you for 25 to 35 years post-retirement. Meanwhile, healthcare and lifestyle costs continue to climb relentlessly.

- The Power of Compounding: Starting early allows your compounding engine to do the heavy lifting. Therefore, small amounts invested in your 20s can comfortably outperform much larger amounts invested under stress in your 40s.

- Market Resilience: A longer time horizon provides a vital safety cushion. Specifically, it gives your equity portfolio the room it needs to recover from short-term market volatility and macro economic cycles.

Recommended Reading on Grey Smiles: What is Retirement Planning and Why Should It Be Done Early in Life?

Step 1: Define Your Financial Retirement Goal

Before crunching any numbers, establish your clear timeline and target lifestyle parameters:

- Establish Your Target Age: Age 60 remains the standard corporate benchmark for retirement in India.

- Project Post-Retirement Living Costs: Map out your future monthly expenses clearly. Ensure you account for core essentials like food, utilities, and housing maintenance alongside lifestyle aspirations like travel.

- Incorporate a Contingency Buffer: Always add a 20% to 30% safety margin to your projected expenses. This buffer safely absorbs unexpected lifestyle or medical surprises.

Step 2: Calculate Your Target Corpus (The 25x Rule)

Estimating your required retirement pool involves a clear, three-step math framework:

- Determine Annual Baseline Expenses: First, multiply your current monthly living expenses by 12.

- Adjust for Inflation: Next, factor in a realistic long-term Indian inflation benchmark of 6% per annum. This projection reveals what those baseline expenses will cost by your target retirement year.

- Apply the 25x Multiplier: Finally, apply the benchmark formula where your Required Corpus = Future Annual Expenses × 25.

This calculation relies on the 4% Safe Withdrawal Rate philosophy. Essentially, pulling out 4% of your total corpus annually allows your principal to remain intact while outpacing inflation.

📊 Illustrative Calculation

- Current Monthly Expenses: ₹50,000

- Time to Retirement: 20 Years

- Future Monthly Expenses (Adjusted at 6% Inflation): ~₹1.60 Lakh

- Future Annual Expenses: ~₹19.20 Lakh

- Total Required Corpus (25x Multiplier): ₹4.80 Crore

Note: Assuming a conservative 10% annualized return during the accumulation phase, your required monthly equity SIP from scratch is approximately ₹62,000. Use a dedicated online financial calculator to map your exact age parameters.

Recommended Reading on Grey Smiles: Smart Strategies to Fill Gaps in Your Retirement Corpus

Step 3: Comprehensive Retirement Planning for Salaried Employees in India

To build your multi-crore corpus successfully, optimize your regular investments across India’s core fixed-income and equity instruments:

1. Fixed Income & Debt Anchors

- Employees’ Provident Fund (EPF): This serves as the primary automated retirement anchor for salaried corporate professionals. Managed via the official EPFO Portal, it offers a highly competitive, government-backed fixed return along with matching employer contributions.

- Voluntary Provident Fund (VPF): This is an excellent tool if you have an extra investable surplus. It allows you to increase your EPF contribution voluntarily up to 100% of your basic pay.

- Public Provident Fund (PPF): A safe, sovereign-backed savings avenue featuring a 15-year lock-in period. Because it offers Exempt-Exempt-Exempt (E-E-E) tax status, it is ideal for building your core, risk-free debt foundation.

2. Market-Linked Equity Growth Engines

- Equity Mutual Funds (SIPs): This stands as the single most effective engine for beating long-term inflation. Focus your core portfolio on diversified large-cap, flexi-cap, and low-cost index funds. Additionally, automate your investments via systematic investment plans (SIPs) and scale up your amounts as your salary grows.

- National Pension System (NPS): A low-cost, highly structured retirement tool. It allows you to select a dynamic blend of equity and debt. Crucially, it unlocks an exclusive, additional tax deduction of ₹50,000 under Section 80CCD(1B).

- Equity Linked Savings Schemes (ELSS): These tax-saving mutual funds qualify under Section 80C. They offer market-linked equity exposure with a brief 3-year lock-in period.

3. Post-Retirement Safety & Distribution

- Annuities: Turning a portion of your corpus into an annuity plan guarantees a steady, lifelong pension stream. However, avoid locking your entire wealth here; keep some liquid growth assets.

- Senior Citizens Savings Scheme (SCSS) & Fixed Deposits: These are high-safety capital preservation vehicles. They protect your money and provide a steady yield during your active retirement years.

Step 4: Master Strategic Asset Allocation

Never invest blindly. Instead, let your age guide your portfolio’s risk exposure using a flexible asset allocation rule of thumb: Target Equity Allocation % = 100 − Your Current Age.

| Current Age | Equity Allocation (Growth) | Debt Allocation (Safety) | Strategy Focus |

|---|---|---|---|

| 30 Years Old | ~70% Allocation | ~30% Allocation | Aggressive Compounding Engine |

| 50 Years Old | ~50% Allocation | ~50% Allocation | Capital Preservation Shift |

Filter in your personal metrics and ensure you rebalance your portfolio once a year to reset your target asset mix. Selling high-flying assets to buy undervalued ones helps maintain your target risk profile.

Recommended Reading on Grey Smiles: Young and Planning Retirement? What You Need to Know About Asset Allocation

Step 5: De-Risk Your Retirement Blueprint

Unplanned life events can easily derail a robust wealth-building strategy. Therefore, protect your capital accumulation phase with these defensive planning pillars:

- Establish a Bulletproof Emergency Fund: Maintain 6 to 12 months’ worth of living expenses in highly liquid vehicles. For instance, a sweep-in savings account or liquid mutual funds will easily cover sudden job transitions.

- Secure Private Health Insurance: Relying solely on corporate group health cover is a critical mistake. Secure an independent family floater health policy early. Subsequently, expand it with a Super Top-Up plan as you age to hedge against steep healthcare inflation.

- Procure Pure Term Life Insurance: Buy a pure term insurance policy if you have dependents or outstanding liabilities. Aim for a sum assured equal to 10 to 15 times your annual income to safeguard your family’s future.

- Eliminate High-Cost Toxic Liabilities: Make it a non-negotiable rule to systematically pay off all high-interest personal loans and credit card debts long before entering retirement.

Step 6: Optimize for Tax Efficiencies

Maximizing your take-home retirement wealth requires careful adherence to structural tax frameworks:

- Section 80C: Fully exhaust your ₹1.5 Lakh annual deduction limit using productive tools like your EPF, PPF, or ELSS funds.

- Section 80CCD(1B): Secure the standalone ₹50,000 tax deduction by actively routing regular investments through the National Pension System.

- Capital Gains Tactical Planning: Long-Term Capital Gains (LTCG) tax applies to equity mutual fund gains exceeding ₹1.25 Lakh per financial year at a flat rate of 12.5%. Consequently, you should work with a certified expert to plan structured, tax-harvested annual withdrawals rather than lump-sum liquidations.

Step 7: Finalize Pension Streams & Estate Planning

True financial independence means ensuring your wealth transfers smoothly according to your wishes. Consider these final steps:

- Track Corporate Benefits: Coordinate regularly with your corporate HR department. This allows you to evaluate your current Gratuity status and accumulated Employee Pension Scheme (EPS) benefits.

- Maintain Updated On-Record Nominations: Ensure up-to-date nominee declarations are explicitly registered across all bank accounts, mutual fund folios, insurance policies, and EPF/NPS profiles.

- Draft a Comprehensive Legal Will: Ensure a clear, legally binding Will is drafted to seamlessly distribute your assets without probate disputes. Additionally, execute a financial Power of Attorney (PoA) to guarantee seamless wealth management in the event of future medical incapacity.

Recommended Reading on Grey Smiles: Myths around Nominee, Joint applicant and a Will

Your Milestone Action Plan by Age

- In Your 20s (The Foundations): Initiate automated, diversified mutual fund equity SIPs immediately. Subsequently, build your core 6-month liquidity emergency buffer and secure a low-premium personal term life insurance policy to kickstart your long-term roadmap for retirement planning for salaried employees in india.

- In Your 30s (The Acceleration): Consistently step up your monthly SIP contributions by at least 10% with every salary appraisal. Additionally, set up a comprehensive, independent family health insurance plan and diversify into systematic NPS or long-term PPF architectures.

- In Your 40s (The Consolidation): Aggressively pay down all outstanding home loans or major liabilities. Then, begin transitioning your asset allocation away from pure equity toward a balanced debt mix while conducting an annual audit to check for gaps.

- In Your 50s (The Transition): Prioritize absolute capital preservation and insulate your portfolios from market shocks. Afterward, finalize a strict, post-retirement household monthly budget and lock in steady pension income via structured debt instruments.

Common Retirement Planning Blunders to Avoid

- Over-relying on Traditional Fixed Deposits: FDs are heavily taxed based on your absolute income slab. Consequently, they routinely fail to beat real, inflation-adjusted living costs over the long run.

- Delaying the Starting Line: Procrastinating your savings by even 5 years dramatically increases the monthly investment amount required to execute successful retirement planning for salaried employees in india.

- Underestimating Medical Inflation: Late-stage healthcare costs climb at a rate much faster than core consumer inflation. Therefore, going without dedicated insurance will quickly deplete your retirement pool.

- Ignoring Post-Tax Projections: Calculating your future income goals without factoring in capital gains taxes will leave you with a noticeable shortfall when you begin withdrawing funds.

Immediate Implementation Checklist

Take charge of your plan right now by checking off these critical action items:

- Document your true baseline monthly living expenses right now.

- Fix your target retirement age and identify your ideal post-retirement lifestyle needs.

- Review your active balances across your corporate EPF, PPF, or NPS accounts.

- Set up or increase your automated equity mutual fund SIP contributions.

- Secure independent personal health insurance and an adequate term plan.

- Set a calendar alert to rebalance your asset allocation once a year.