The greatest threat to many senior citizens today does not come from strangers. Instead, it often comes from misplaced trust. Many parents completely transfer their homes and lifelong savings to their children. They believe they will be cared for in their golden years. However, they often realize too late that their voluntary choices were the result of subtle persuasion. Financial exploitation, emotional neglect, and elder abuse by family members are rising sharply across India. Yet, social stigma and emotional dependence keep many victims silent. Consequently, as life expectancies rise, tomorrow’s seniors must shift toward legally enforceable choices.

Common Mistakes Senior Citizens Should Avoid

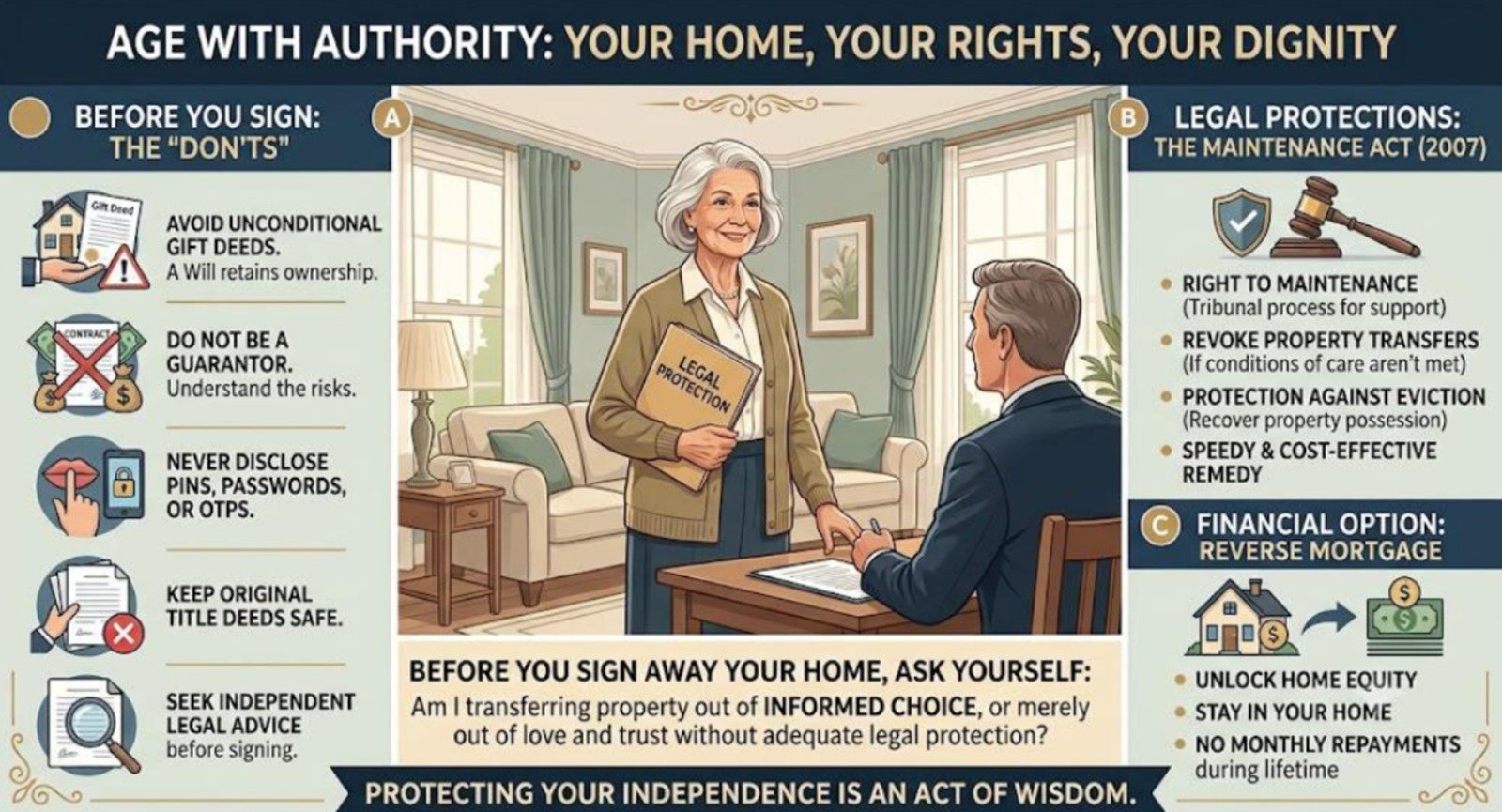

The legal framework in India is gradually evolving to provide stronger protections. Nevertheless, the most effective safeguard remains informed, preventive decision-making. You can protect your autonomy by avoiding these common oversights:

- Ignoring Early Warning Signs: Never overlook early patterns of emotional or financial manipulation by family members.

- Executing Unconditional Gift Deeds: Transferring property unconditionally leaves you highly vulnerable. Therefore, consider executing a conditional Gift Deed or a robust asset protection plan through a registered Will. For structured guidance on organizing your estate, review the forthcoming foundational checklists on greysmiles.com to secure your spouse’s future. To ensure you don’t compromise your immediate safety nets, always be aware of the common emotional mistakes to avoid with your retirement fund.

- Guarantor Vulnerabilities: Avoid acting as a guarantor for children’s loans. This is because you may face severe financial liabilities if they default.

- Convenience Joint Accounts: Do not add a relative’s name to your primary property deeds or bank accounts merely for administrative convenience. Instead, use explicit nomination facilities.

- Surrendering Original Documents: Never hand over original title deeds or vital financial documents unless mandated by a verified legal process.

- Relying on Oral Assurances: Verbal promises regarding future care and medical maintenance are incredibly difficult to enforce. Consequently, you should always reduce care arrangements to writing.

- Outdated Estate Plans: Review and update your succession documents after every major life milestone.

- Exposing Security Credentials: Never disclose passwords, banking PINs, or OTPs to anyone. This includes your children and grandchildren.

- Skipping Independent Counsel: Always seek independent legal advice before signing any document that alters your ownership rights.

Protection Under the Law

Parliament and various state divisions have enacted specific statutes to preserve the dignity of senior citizens. Key legislative provisions include:

- Maintenance and Welfare of Parents and Senior Citizens Act, 2007: This landmark law enables seniors to claim a monthly maintenance allowance from legal heirs. Crucially, Section 23 allows the revocation of property transfers if children fail to provide basic amenities. Furthermore, you can access the complete statutory text through the official India Code Portal.

- Bharatiya Nyaya Sanhita (BNS) / Indian Penal Code: This framework provides strict criminal remedies against targeted elder abuse, cheating, and intentional abandonment.

- Protection of Women from Domestic Violence Act, 2005: This Act offers elderly women critical protection from physical or economic abuse within a shared household. Moreover, recent rulings emphasize that an elderly parent’s right to live peacefully overrides a relative’s secondary right of residence.

- Transfer of Property Act, 1882: This law validates the structuring of conditional transfers. As a result, life interests remain explicitly with you.

- Indian Succession Act, 1925: This statute governs the formal execution and probate of Wills. Thus, it allows you to control how your assets are managed.

- Registration Act, 1908: This Act dictates the necessary compliance rules to ensure your property actions carry full legal weight.

- Banking and Reserve Bank of India (RBI) Regulations: These rules mandate absolute protection features for senior citizens. For example, they guarantee simplified doorstep banking and streamlined nomination updates.

Reverse Mortgage: Turning Your Home into Financial Security

For asset-rich but cash-poor seniors, a Reverse Mortgage Loan (RML) is a vital financial tool. It allows eligible senior homeowners to unlock the equity built up in their self-occupied residential property. The bank pays you a regular monthly stream or a lump sum based on the value of your home. Meanwhile, you continue to own and occupy the property during your lifetime. The loan is settled by the bank later through the sale of the house. Alternatively, your heirs can clear the loan if they choose to retain the asset. For a deep-dive breakdown of how this option stacks up against traditional retirement withdrawals, explore the lifestyle transition planning resources available via our foundational look at What are Mutual Funds for Retirement?.

Financial Security and Welfare Schemes

Seniors without active family support can access extensive welfare benefits structured by both Central and State governments:

1. Financial Stability & Pensions

- Indira Gandhi National Old Age Pension Scheme (IGNOAPS): This scheme provides monthly pension support targeted at elderly citizens living below the poverty line.

- Senior Citizens Savings Scheme (SCSS): This is a secure, government-backed investment avenue. Consequently, it offers robust, high-yield quarterly interest payouts for retirees.

- Shravan Bal Seva State Pension Scheme: This is a specialized, Maharashtra-specific welfare program that delivers direct financial assistance to destitute senior citizens.

2. Healthcare & Medical Security

- Ayushman Bharat PM-JAY (70+ Coverage): This program provides free health insurance coverage up to ₹5 Lakh per year for all senior citizens aged 70 and above. In addition, it is completely independent of family income tiers. You can check structural eligibility parameters at the official Ayushman Bharat PM-JAY Portal.

- National Programme for Health Care of the Elderly (NPHCE): This initiative mandates dedicated geriatric clinics and subsidized medication pipelines.

- Atal Vayo Abhyudaya Yojana (AVYAY): This is a flagship umbrella initiative focusing on holistic elder care. For instance, it runs assistive camps and funds dedicated regional support systems.

3. Rehabilitation & Community Care

- Elderline Services (14567): This is a national, toll-free helpline operating under AVYAY. It offers immediate emotional support and legal guidance for seniors in distress.

- Rashtriya Vayoshri Yojana (RVY): This program distributes free physical aids, such as wheelchairs and spectacles, to low-income seniors.

- Chief Minister Vayoshree Yojana & Teerth Darshan Schemes: These state-level programs provide targeted wellness financial support. Furthermore, they offer fully subsidized pilgrimage facilitation.

Institutional Care: Due Diligence

Specialized senior living communities are expanding rapidly across India. However, choosing the right space requires strict due diligence. If you are tracking this transition, be sure to reference our operational roadmap outlining What to Look for in a Senior Living Community. Therefore, families must proactively verify:

- Legal Status: Confirm the facility’s explicit registration under local municipal bodies.

- Medical Infrastructure: Evaluate their round-the-clock nursing access and tie-ups with emergency trauma hospitals.

- Contractual Transparency: Thoroughly review the admission agreement. Specifically, pay careful attention to escalating monthly maintenance fees and security deposit refund clauses.

Preserving Your Independence

Although legal remedies exist to resolve family disputes, prevention remains vastly superior to litigation. Safeguarding your financial assets is not a sign of mistrust. Rather, it is a responsible step to ensure your later years are lived with dignity.

Before you sign over your home or clear out your savings, pause and ask yourself one definitive question:

“Am I transferring this asset out of informed choice with legal protection, or am I acting entirely on emotional trust, leaving myself completely vulnerable?”