Retirement should mean absolute financial security for families after a lifetime of hard work. However, millions of legal heirs across India discover only after a tragedy that sizeable life savings are trapped out of reach. Billions of rupees lie completely forgotten in dormant bank accounts, un-transferred provident fund balances, untouched insurance payouts, and static postal savings schemes. This growing crisis stems from low financial literacy, poor documentation habits, and historically complex institutional frameworks. This comprehensive guide breaks down the true scale of India’s unclaimed retirement wealth crisis, identifies the primary structural roadblocks, and delivers actionable blueprints for both retirees and beneficiaries to reclaim what is rightfully theirs.

Table of Contents

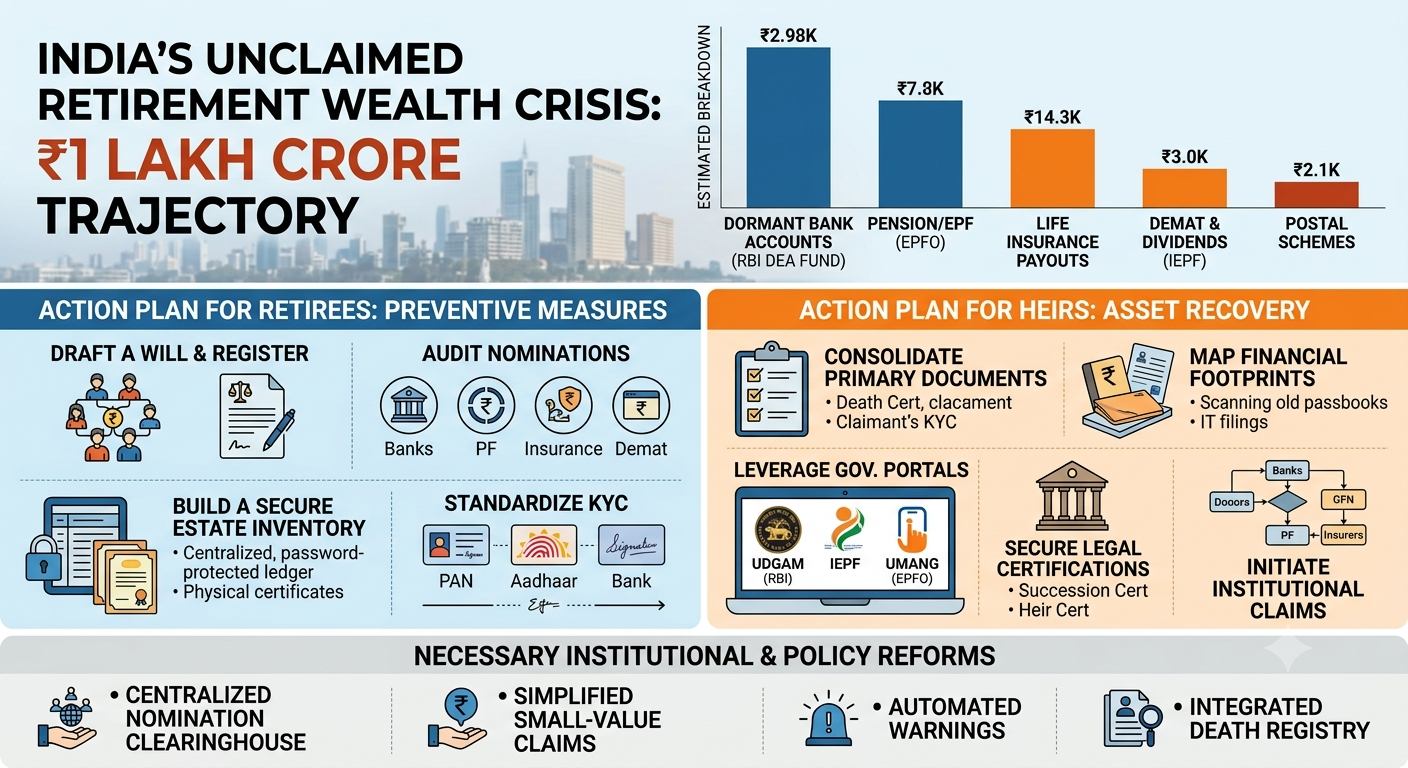

1. The Scale of Unclaimed Retirement Wealth in India

Estimates indicate that the cumulative pool of unclaimed wealth in India has breached the staggering threshold of ₹1 Lakh Crore. This massive financial void spans multiple legacy asset classes, severely disrupting the financial stability of surviving dependents:

- Dormant Bank Accounts & Fixed Deposits: Savings and term deposits automatically transition into an inactive state following 10 consecutive years of zero user-initiated transactions. These funds are eventually transferred to the RBI’s Depositor Education and Awareness (DEA) Fund.

- Unclaimed Demat Holdings & Dividends: Investor shares, physical equity certificates, and corporate dividends remain completely frozen when underlying trading accounts go cold. Unclaimed dividends are legally transferred to the Investor Education and Protection Fund (IEPF) after seven consecutive years.

- Provident Fund & Pension Balances: Millions of salaried professionals neglect to transfer their Employee Provident Fund (EPF) balances during corporate transitions. Following retirement or death, these non-operational accounts cease earning interest, leaving massive corpuses stranded within the EPFO ecosystem.

- Unpaid Life Insurance Claims: Policy payouts regularly stall when insurers fail to track down changing addresses of beneficiaries, or when legal heirs lack clarity on existing policy numbers and claim procedures.

- Post Office Savings Schemes: Traditional long-term instruments like the Public Provident Fund (PPF), National Savings Certificates (NSC), and basic postal deposits regularly go missing from family ledgers because nominees were either never registered or never informed.

2. Key Challenges in Transferring Unclaimed Wealth

The unclaimed wealth crisis persists due to deep legacy bottlenecks that make asset recovery incredibly painful for grieving families:

- Severe Communication Gaps: A vast majority of account holders fail to securely document or share comprehensive lists of financial assets with their immediate families, leaving heirs entirely unaware that the money even exists.

- Nomination Fault Lines: Outdated asset portfolios frequently feature missing nominees, minor nominees who have since aged without updated documentation, or complex joint holdings lacking explicit “Either or Survivor” operational clauses. For a deeper breakdown on clearing up these ownership misunderstandings, read our comprehensive guide on the myths around nominees, joint applicants, and wills.

- Bureaucratic & Legal Hurdles: When legacy assets cross specific statutory thresholds, financial institutions demand exhaustive legal validations. Families are forced to navigate the civil court systems to secure highly regulated Succession Certificates, Letters of Administration, or Probate Orders.

- KYC & Identity Mismatches: Minor inconsistencies in legacy paper documentation—such as misspelled names, old residential addresses, or mismatched dates of birth on foundational identity cards (PAN, Aadhaar)—frequently trigger compliance blocks during institutional verification.

- Highly Fragmented Ecosystems: Legal heirs are forced to deal with completely isolated verification systems, varying compliance protocols, and decentralized online portals across individual banks, post offices, the EPFO, multiple insurance firms, and judicial bodies.

3. Action Plan for Retirees: Preventive Measures

Proactive asset management is the absolute best insurance policy you can give your dependents. Retirees should optimize their portfolios using these core steps:

- Draft and Register a Will: Document a legally robust Will detailing asset distribution to eliminate family ambiguity. Registering the final document at your local sub-registrar’s office drastically minimizes future probate litigation risks.

- Audit Institutional Nominations: Explicitly update primary and secondary nominees across all active savings accounts, insurance frameworks, demat repositories (NSDL/CDSL), and long-term retirement accounts. Ensure you understand how these roles function alongside your final estate distribution goals by reviewing strategic retirement estate planning strategies.

- Build a Centralized Estate Inventory: Create a highly secure master ledger containing bank account numbers, customer IDs, insurance policy codes, active depository client IDs, secure login hints, and the exact physical location of original certificates.

- Establish a Trusted Point of Contact: Safely share your master financial inventory and clear structural instructions with a designated executor or a trusted family member.

- Standardize Modern KYC Profiles: Ensure that your name, date of birth, and primary signatures match flawlessly across your active PAN, Aadhaar cards, and financial asset registries to avoid structural roadblocks later.

4. Action Plan for Heirs: Asset Recovery Process

If you need to recover a deceased family member’s stranded savings, follow this structured roadmap:

- Consolidate Primary Documents: Gather authentic physical records, including the official Death Certificate, the claimant’s current KYC profiles (PAN and Aadhaar cards), direct legal relationship proof, and any registered Wills or Nominee declarations.

- Map Out Past Financial Footprints: Systematically audit old physical statements, historical bank passbooks, past income tax filings (ITR), insurance premium receipts, and direct physical correspondence from financial institutions.

- Leverage Government Search Engines: Utilize centralized verification portals such as the RBI’s UDGAM platform for dormant bank accounts, the IEPF registry for long-lost equity dividends, and the integrated UMANG mobile platform for tracing stranded EPF corpuses.

- Secure Necessary Legal Certifications: For high-value legacy accounts devoid of direct nomination paths, approach local revenue officials or the relevant district civil court to secure a formalized Legal Heir Certificate or a Succession Certificate.

- Initiate Institutional Claim Workflows: Submit your formal request directly through the specific digital claim modules hosted by the respective banking partners, insurers, or asset management companies.

5. Necessary Institutional and Policy Reforms

Resolving this national asset crisis permanently requires deep systemic upgrades from regulatory bodies and policymakers:

- A Centralized Nomination Clearinghouse: Regulators should introduce a unified national registry linking cross-institutional nominations across banks, mutual funds, insurance providers, and depositories to let heirs discover assets via a single query.

- Simplified Small-Value Claim Processing: Standardizing and lowering legal documentation benchmarks for low-to-mid tier financial claims would radically cut down a family’s dependency on delayed civil courts.

- Automated Institutional Warnings: Mandate financial companies to initiate proactive communications (via automated text alerts, phone calls, and physical mailers) to both owners and registered nominees well before an account shifts into an inactive state.

- Integrated Death Registry Systems: Build automated digital bridges between local municipal death registration systems and the broader financial network to immediately trigger beneficiary notifications when an account holder passes away.

Conclusion: Take Control of Your Financial Legacy

Unclaimed family wealth across India is more than just a macroeconomic statistic—it represents a heavy, entirely preventable emotional and financial burden for surviving heirs. Mitigating this issue requires a two-pronged approach: individuals must take immediate personal responsibility by updating institutional nominations and maintaining clean estate records, while regulatory frameworks must continue evolving toward simplified, unified digital claim models. Securing your hard-earned wealth is an ongoing obligation; start auditing your active accounts today to protect the future of the people you care about most.