Published by: Kartikey Gupta

AMFI,

SEBI,

and the Income Tax Department, this article offers a tactical roadmap to mastering these powerful investment vehicles. Whether you are aiming to balance aggressive equity growth or secure steady income, understanding the architecture of retirement-focused mutual funds is the crucial first step toward financial freedom in your second innings.

1. What are Mutual Funds for Retirement?

Retirement mutual funds are specialized financial products engineered to help individuals save, grow, and manage capital over the long term specifically to fund their post-employment life. They operate on a simple yet effective model: pooling funds from thousands of investors to invest in a diversified mix of equities (stocks), debt (bonds), and other dynamic securities. Under the guidance of professional fund managers, these schemes have two primary objectives: aggressive accumulation and growth during your working years, followed by structured income generation once you retire. Unlike generic savings, these are goal-based investing vehicles aligned with a specific retirement horizon.

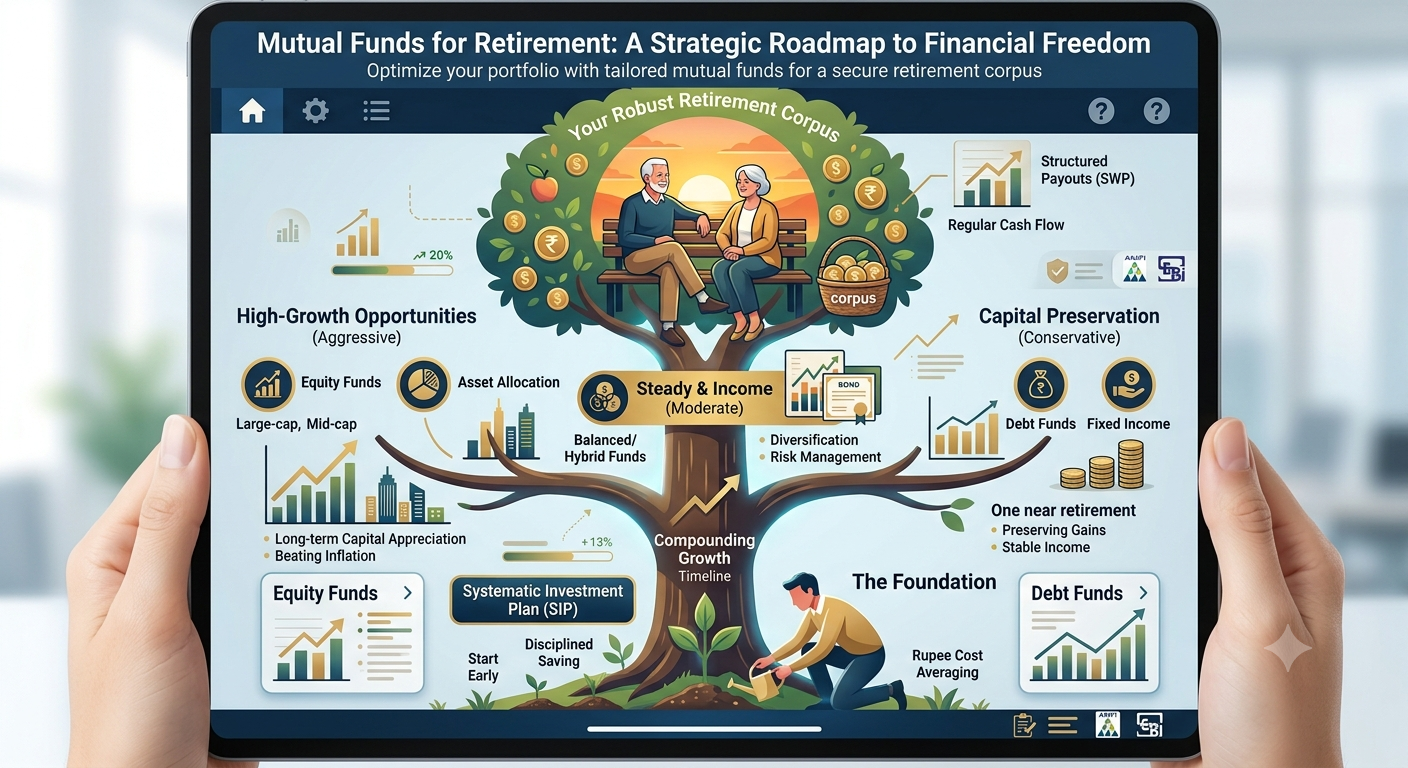

2. Understanding Your Retirement Investment Options

Not all mutual funds are structured the same. Your asset allocation—the balance between different types of funds—is the primary driver of both risk and return.

Large-cap Fund: Stability and Steady Growth

These funds invest in the top 100 established Indian companies by market capitalization. The focus here is on long-term stability. While they may not offer explosive growth, they provide steady returns and tend to be less volatile during market downturns. They are the bedrock of most retirement portfolios.

Mid-cap Fund: Capturing High Growth Potential

These target mid-sized companies (generally ranked 101–250 by market cap) that are transitioning toward becoming industry leaders. They carry higher growth potential than large-caps but come with moderate to high volatility. These are excellent for younger investors looking to aggressively build their corpus.

Debt Fund: Steady Income and Capital Preservation

Debt funds invest in fixed-income instruments, including government securities, corporate bonds, and debentures. Their main goal is to provide steady income and capital preservation with lower volatility than equity. These are essential as you approach retirement age to lock in gains.

Balanced / Hybrid Fund: The Moderate Route

Hybrid funds mix equity and debt in varying proportions. They aim for both capital appreciation (from the equity component) and regular income/stability (from the debt component). This “all-in-one” approach is suitable for investors with a moderate risk tolerance who want structured asset allocation without managing multiple funds.

💡 Smart Strategy: Use Voluntary Provident Fund (VPF) as your fixed-income anchor and complement it with an aggressive compounding mutual fund strategy.

3. Core Features of Mutual Funds for Retirement

What makes mutual funds for retirement uniquely suited for goal-based investing? It comes down to structural parameters that enforce discipline.

- Automatic Investment via SIPs: Regular, mandatory contributions through Systematic Investment Plans (SIPs) encourage disciplined saving and use rupee cost averaging to smooth out market volatility.

- Professional Asset Allocation: Fund managers align the fund’s holdings to its stated retirement objective, optimizing the equity/debt balance to maximize returns within a predefined risk profile.

- Range of Risk Profiles: From conservative debt schemes for near-retirees to aggressive small/mid-cap schemes for new investors, a mutual fund ecosystem offers options for every life stage.

- Structured Payout Plans: Many retirement-specific funds offer specialized Systematic Withdrawal Plans (SWP) or structured payout options designed to provide consistent monthly cash flows once you retire.

- Dynamic Solutions: Some “pension schemes” within mutual funds incorporate dynamic asset allocation (switching risk levels automatically based on your age) and may include loyalty additions, though these vary significantly by product and expense ratio.

4. Strategic Benefits: Building and Accessing Your Corpus

Navigating how Millennials and GenZ view career and retirement planning shows a high demand for flexibility—a key strength of the mutual fund structure.

Potential for High-Velocity Growth

The primary benefit is equity exposure. Over multi-decade periods, equity has historically outperformed inflation and traditional fixed deposits by a significant margin, creating the sizable corpus necessary to beat healthcare and lifestyle inflation.

Predictable Post-Retirement Cash Flow

Debt and hybrid funds can be structured with a Systematic Withdrawal Plan (SWP) to supply regular payouts in retirement. Unlike annuities which lock your corpus away, SWPs provide cash flow while leaving your core principal potentially exposed to continued (though lower-risk) growth.

Flexibility and Full Control

Mutual funds offer unparalleled flexibility. You have the ultimate control over which funds you select, how much you invest (via SIPs), when you increase contributions, and, crucially, you have the ability to switch funds (subject to rules and tax) as your risk tolerance changes. This contrasts sharply with many rigid pension products.

Specialized Tax Advantages

Specific mutual fund schemes designed as “pension plans” may be eligible for tax deductions under Section 80C or similar provisions of the Income Tax Act (confirm current law). Understanding taxation on your investments is vital to maximizing net returns.

5. Ideal Investor Profiles: Who Should Invest

Mutual funds for retirement are suitable for a wide range of investors, provided they have a long-term goal. Consider this vehicle if you are:

- Goal-Based Savers: Individuals who want to specifically build and track a dedicated, isolated retirement corpus rather than generic savings.

- Passive/Disciplined Savers: Long-term investors who prefer automated monthly contributions (SIPs) that enforce fiscal discipline and reduce emotional decision-making.

- Diversification Seekers: Investors who know they need equity and debt but do not have the time, knowledge, or large capital required to independently build a well-diversified stock and bond portfolio.

- Strategy-Oriented Planners: Investors who want to actively adjust their equity/debt ratio as they approach retirement, moving capital strategically from high-growth mid-caps to stable large-caps and eventually debt funds.

6. Critical Considerations Before You Invest

Blindly investing in high-performing funds is a high-risk strategy. Succeeding with retirement mutual funds requires strict adherence to personalized financial mapping.

- Define Your Target Corpus: Calculate your retirement age, desired post-retirement lifestyle, and projected income needs (accounting for inflation) to determine your precise financial target.

- Assess Risk Tolerance (Emotional and Capital): How much comfort do you have with market volatility? Setting the correct equity/debt balance is more important than selecting the “best” fund.

- Map Your Time Horizon: A longer time horizon (15+ years) allows a portfolio to absorb higher equity risk (small/mid-caps). Near-retirement horizons require a portfolio heavy in debt and stable large-caps.

- Audit Costs (Expense Ratio & Exit Load): High internal costs (Expense Ratio) can silently reduce your final corpus by lakhs over decades. Understand the exit loads (fees for premature withdrawal). High performance must always be balanced against low costs.

- Review Regulatory Lock-ins and Rules: While standard funds are liquid, some specialized “Retirement/Pension Schemes” have mandatory lock-in periods and strict withdrawal or annuity mandates. Understand these exit rules *before* you invest.

- Commit to Regular Reviews: Your life changes. Marriage, children, job changes, and major medical events should always trigger a review and rebalance of your retirement mutual fund strategy to stay aligned with your original goals.

7. Vital Notes on Indian Mutual Fund Taxation

It is imperative to understand that the tax treatment of mutual funds in India depends entirely on the specific product type (Equity-oriented vs. Debt-oriented), your holding period (Short-Term vs. Long-Term), and current legislation.

- Contribution Phase (Deductions): Contributions to certain recognized pension schemes may be eligible for deductions under Section 80C, 80CCC, or 80CCD (check current limits and specific applicability).

- Withdrawal Phase (Taxation): Tax on withdrawals, annuity payouts, and accumulated capital gains differs vastly between equity-oriented, hybrid-oriented, and debt-oriented funds. Equity gains are generally taxed as Capital Gains (Short/Long term), while annuity income from some pension products is taxed at your slab rate.

- Consult official sources: Do not rely on generic examples. Taxation is complex and highly individualized. Always verify the latest rules and statutory limits directly with the Income Tax Department or a certified tax advisor.

Wrapping up: The Power of Intentional Self-Direction

Choosing the right mutual funds for retirement is not a one-time event; it is a long-term strategic commitment to your future financial freedom. Success requires four components: (1) absolute clarity on your goals, (2) highly disciplined SIPs, (3) a personalized asset allocation that respects your risk tolerance, and (4) continuous periodic monitoring. By utilizing the innate power of diversification, professional management, and systematic compounding, you can build a formidable retirement corpus. Leverage these dynamic tools to take intentional control over your legacy.

A Vital Note: Specific product features—including lock-ins, annuity mandates, sum‑assured protections, loyalty additions, free switches, surrender values, and specialized tax benefits—differ vastly across standard mutual funds versus insurance‑based retirement plans. Always read the scheme documents carefully, cross-verify all benefits, and seek professional financial and tax advice before executing your strategy.