This comprehensive guide outlines how to build a resilient cash-flow engine designed specifically for the Indian economic and tax landscape using structured maturity intervals.

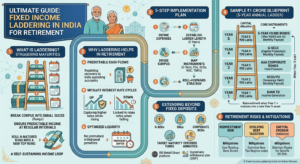

What is Fixed Income Laddering?

Instead of deploying a massive sum into a single 5-year Fixed Deposit (FD) or keeping it entirely in a low-yield savings account, you break your capital into smaller, structured slices called rungs.

As each lower rung matures, it supplies immediate cash to fund your living expenses or is rolled over into a new long-term rung at the top of the ladder. This creates a self-sustaining loop of reliable income.

Why Fixed Income Laddering Helps in Retirement

Surviving a 25- to 30-year retirement window requires moving beyond static savings. Designing a dynamic maturity timeline delivers several immediate structural benefits:

- Predictable Cash Flows: By organizing rungs to mature at specific times of the year, you create natural intervals to replenish your daily transaction accounts without needing to constantly liquidate long-term investments. For deeper baseline planning, read our guide on mapping pension plans versus fixed returns.

- Mitigation of Interest-Rate Cycles: If India’s macro-interest rates rise, you will regularly have cash from maturing rungs ready to capture those higher yields. If interest rates fall, the top rungs of your ladder remain safely locked into the higher rates of previous years.

- Optimized Liquidity Control: Emergency cash needs are met naturally by upcoming maturities, protecting you from premature withdrawal penalties on long-term deposits.

- Behavioral Insulation: Knowing exactly where your next 12 to 36 months of living expenses are coming from prevents panic selling of your equity or growth assets during volatile stock market corrections.

How to Implement Fixed Income Laddering Efficiently (Step-by-Step)

Building a dependable fixed-income matrix involves a methodical approach tailored to your specific monthly requirements.

Step 1: Define Your True Floor Expenses

Before allocating a single rupee, map out your annual cash outflow. Separate your budget into essential living expenses (food, utilities, healthcare inflation, insurance premiums) and discretionary expenses (travel, leisure). Your strategy for fixed income laddering in India should be designed primarily to cover your essential floor expenses, plus an emergency buffer.

Step 2: Establish Ladder Length and Spacing

A standard blueprint for Indian retirees is a 5-year ladder with annual rungs. If your lifestyle demands hyper-frequent income distribution, you can configure the rungs at 6-month or 12-month intervals to align with specific cash-flow needs.

Step 3: Divide and Allocate Your Corpus

Determine whether to allocate capital equally across all rungs or weight them to match your spending profile. An equal allocation gives you a symmetrical roll-forward cycle, whereas a front-weighted allocation provides a larger safety cushion in the initial years of your retirement transition.

Step 4: Map Instruments to Corresponding Rungs

Select your financial products based on institutional safety and timeframe suitability:

- Short-Term (Rungs 1-2): High-yield savings accounts, capital-safe Bank FDs, or liquid options.

- Medium-to-Long Term (Rungs 3-5+): Sovereign gold/dated bonds, Senior Citizens Savings Scheme (SCSS), National Savings Certificates (NSC), or highly rated corporate papers.

Step 5: Execute the Roll-Forward Strategy

When Rung 1 matures at the end of Year 1, you have a choice based on your financial position:

- Consume: Use the cash to fund the upcoming year’s lifestyle requirements.

- Roll Forward: If your other income sources (like rental income or dividends) covered your expenses, reinvest that matured capital into a brand new 5-year rung at the top of the ladder.

Step 6: Conduct an Annual Calibration

Review your entire asset structure once a year. Assess changes in the prevailing tax laws, adjustments to your lifestyle, and the performance of your complementary growth assets to rebalance your portfolio efficiently.

Sample ₹1 Crore Practical Fixed Income Laddering Blueprint

To illustrate how this works, consider a retiree deploying a ₹1 Crore fixed-income corpus into a balanced, 5-rung annual layout designed for maximum safety and steady cash generation:

| Rung Timeline | Capital Allocation | Suggested Core Instruments | Primary Operational Role |

|---|---|---|---|

| Year 1 Maturity | ₹20 Lakhs | High-Quality Scheduled Bank FD (with monthly or quarterly interest payout) | Immediate income generation to fulfill daily living expenses. |

| Year 2 Maturity | ₹20 Lakhs | Senior Citizens Savings Scheme (SCSS) or Post Office Time Deposits | Guaranteed sovereign yield backing your intermediate cash reserves. |

| Year 3 Maturity | ₹20 Lakhs | Short-Duration Corporate Bonds (AAA Rated Only) | Capturing a yield premium over traditional bank deposits with minimal credit risk. |

| Year 4 Maturity | ₹20 Lakhs | Government Securities (G-Secs) or Long-Term Public Sector Bonds | Absolute sovereign capital protection as the money sits mid-ladder. |

| Year 5 Maturity | ₹20 Lakhs | 5-Year Bank Fixed Deposits or RBI Floating Rate Savings Bonds | Maximum yield lock-in at the apex rung of the fixed-income strategy. |

The Operational Cycle: At the end of Year 1, the first ₹20 Lakh tranche matures. You utilize the interest payouts for your expenses. You then move the Year 2 rung down to fill the Year 1 slot, shift every subsequent rung down by one year, and deploy the fresh capital from your matured rung into a brand new Year 5 asset at the current market rate.

Extending Fixed Income Laddering Beyond Fixed Deposits

Relying solely on standard bank fixed deposits exposes your retirement to structural limitations. Modern fixed-income management allows you to look at alternative structures to improve diversification:

1. Sovereign G-Sec and Dated Bond Ladders

Instead of commercial banks, you can purchase individual Government of India Dated Securities (G-Secs) or State Development Loans (SDLs) directly via the RBI Retail Direct platform. These allow you to build zero-default-risk ladders spanning anywhere from 1 to 30 years, locking in predictable coupon payouts.

2. High-Grade Corporate Non-Convertible Debentures (NCDs)

For tranches of your capital positioned in Years 3 through 5, you can step up your yield by purchasing NCDs issued by public sector undertakings (PSUs) or blue-chip corporations. Stick rigidly to CRISIL/ICRA AAA or AA+ rated instruments to ensure the credit risk remains firmly under control.

3. Target Maturity Funds (TMFs) and Systematic Withdrawal Plans (SWPs)

Target Maturity Funds are passive debt index funds that track a specific underlying index of G-Secs or PSU bonds and feature a defined maturity date. By purchasing a series of TMFs that mature in consecutive years, you build a synthetic, low-cost ladder. You can layer a Systematic Withdrawal Plan (SWP) on top to automate monthly cash drops directly into your bank account.

4. Slipped Annuity Tranches

Instead of buying a single massive annuity policy at age 60, split your purchase into deferred tranches. Purchasing smaller immediate or deferred annuity contracts at ages 60, 63, and 66 allows you to lock in different annuity rates, capitalize on higher payout percentages as your age advances, and mitigate timing risk.

Retirement Risks & Tactical Mitigations

While laddering provides exceptional structural balance, an effective long-term strategy must explicitly account for Indian economic shifts and tax frameworks:

Reinvestment Realities

- The Risk: Maturing rungs might hit the market during an extended low-rate cycle, forcing you to reinvest your capital at lower yields.

- The Mitigation: Always include floating-rate instruments (such as the RBI Floating Rate Savings Bonds, which adjust periodically based on National Savings Certificate rates) within your broader capital allocation.

Evolving Indian Debt Taxation

- The Risk: Changes in tax laws can impact your net yields. For instance, specified debt mutual funds purchased after April 1, 2023, do not receive long-term capital gains (LTCG) indexation benefits; instead, all gains are treated as short-term capital gains (STCG) and taxed at your progressive income slab rate.

- The Mitigation: Optimize your withdrawals based on the tax regimes available to you. Under the default New Tax Regime, individuals with total taxable income up to ₹12 Lakhs can qualify for full tax exemptions through updated Section 87A rebate limits. You can review current slab thresholds directly via the official Income Tax Department of India web portal to verify tax brackets for interest earnings.

Capital Inflation Erosion

- The Risk: A rigid fixed-income portfolio can lose purchasing power over a multi-decade retirement due to rising consumer inflation.

- The Mitigation: Never allocate 100% of your net worth to fixed income. Maintain a distinct growth layer—comprising 20% to 30% of your total wealth—invested in diversified equity mutual funds, hybrid options, or index tracking funds to expand your capital base over time. For handling price increases on medical care, review our specific deep-dive on managing healthcare inflation in India.

Your Day-One Checklist to Start

Conclusion

Fixed-income laddering offers a highly effective, straightforward framework for retirees seeking to balance liquidity, yield optimization, and portfolio safety. By moving past static single-deposit strategies and spreading capital across staggered maturities—including bonds, secure corporate papers, and automated debt instruments—you can build a reliable cash-flow system that protects your financial independence throughout your retirement.