1. Demographics and Workforce Participation

India’s macro-economic blueprint is anchored by its unmatched demographic dividend. The sheer volume of young individuals entering digital environments is reshaping how retirement trends are quantified across global markets:- A Digitally Connected Workforce: India has scaled past 600 million active internet users, with the vast majority comprised of Millennials and Gen Z individuals. This interconnected baseline directly influences how they gather financial intelligence and consume wealth-management tools.

- Workforce Dominance: According to data from the Ministry of Labor and Employment, youth aged between 15 and 29 account for approximately 34% of the total aggregate workforce in India. This concentration means their collective preferences dictate macro market movements.

2. Shifting Attitudes Toward Modern Work

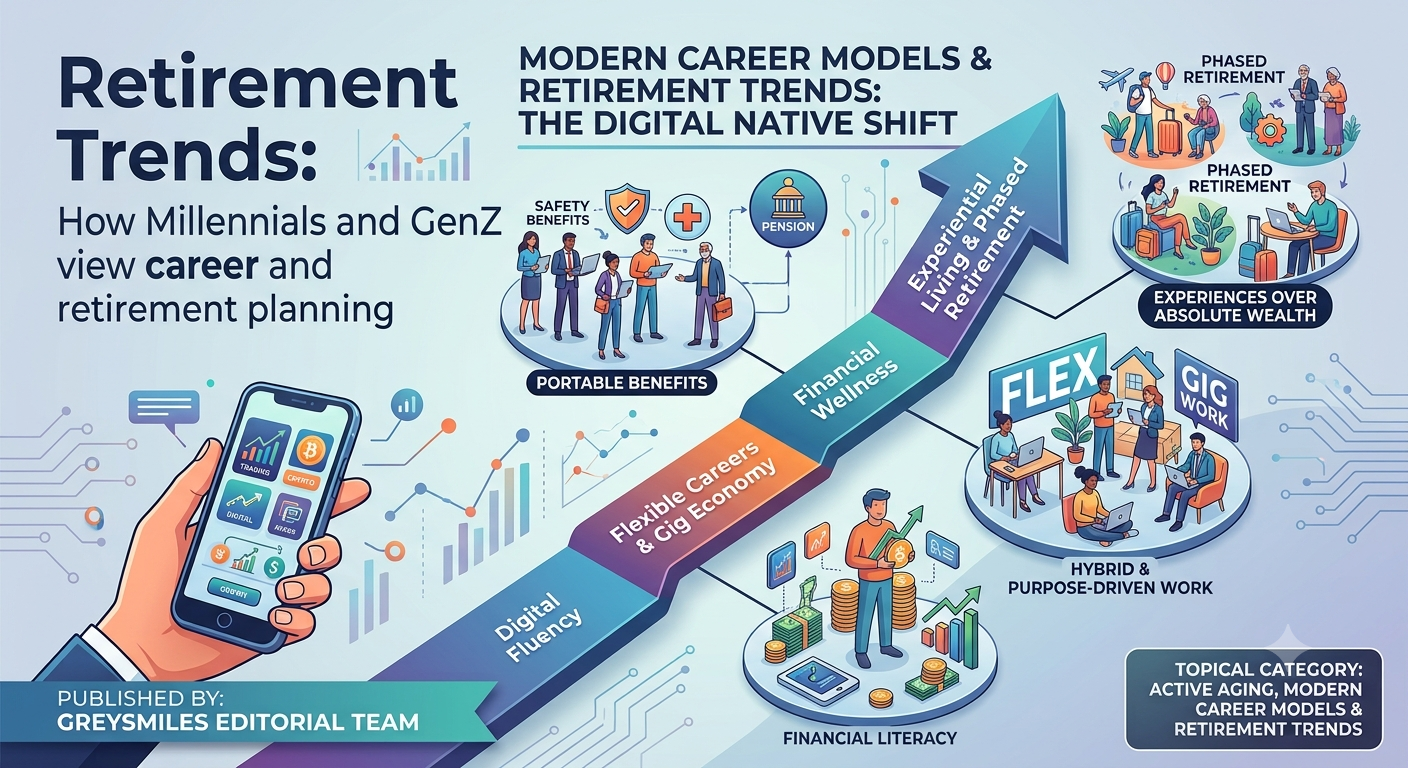

The conventional structure of the 9-to-5 corporate grind is being systematically dismantled. When analyzing how Millennials and GenZ view career and retirement planning, their concept of daily employment directly informs their timeline for financial independence:- The Imperative for Flexibility: Landmark industrial studies indicate that 70% of Millennials and Gen Z professionals in India explicitly prefer job offers that provide structural, flexible work arrangements. The post-pandemic acceleration of hybrid and remote architectures is now a non-negotiable benchmark for talent retention.

- Purpose-Driven Professional Sectors: Data indicates that roughly 67% of the younger workforce is actively willing to accept a compromised or lower initial salary baseline in exchange for roles that explicitly align with their ethics, societal goals, and personal values. This generational alignment is driving massive talent migration into renewable energy grids, tech-enabled healthcare ecosystems, and high-impact non-profit organizations.

3. Financial Literacy and Digital Planning Ecosystems

Younger investors are bypassing traditional, opaque legacy banking portals in favor of agile, transparent, and direct fintech architectures. This structural pivot highlights how modern retirement trends favor automated self-direction over passive delegation.- Sustained National Pension Growth: Institutional metrics from the National Pension System (NPS) showcase that the aggregate subscriber footprint scaled past 48 million, highlighting a notable, recurring influx of retail account creations originating from younger demographics seeking structured wealth compounding.

- The Fintech Disruption Engine: Micro-investing apps and localized fintech platforms have democratized equity market exposure. With major platforms logging user bases exceeding 100 million individuals, young Indians are independently building financial literacy, experimenting with options strategies, and executing long-term investment architectures from their mobile devices.

4. The Rise of Alternate Gig Work Models

The steady rise of the independent contractor and consultant class underscores a deep structural change in workforce patterns. The traditional boundary between a singular employer and a lifelong employee has officially dissolved.- The Macro Scale of the Gig Economy: Strategic industry evaluations from the Boston Consulting Group alongside the Ministry of Labour estimate India’s standalone gig economy valuation scale. With over 15 million independent professionals actively optimizing multi-client portfolios, Millennials and Gen Z form the undisputed operational core of this transformation.

- The Demand for Portable Benefits: As independent working structures solidify, alternative welfare requirements are surfacing. Comprehensive operational surveys highlight that 60% of active gig workers are hunting for specialized, portable financial benefits—most notably corporate retirement savings models that remain entirely detached from a single employer anchor.

5. Evolving Retirement Perceptions: Experiences Over Absolute Wealth

The ultimate end-game of the professional lifecycle is being completely reimagined by the modern workforce:- Deconstructing the Hard Stop: In sharp contrast to old-world models, macro financial tracking surveys reveal that 78% of Millennials and Gen Z actively prefer a gradual transition into retirement. Rather than a abrupt complete stop at age 60, younger generations choose a phased slowdown, shifting down into consultative micro-roles, advisory positions, or entrepreneurial ventures.

- Prioritizing Experiential Runways: Cultural indicators demonstrate that 55% of younger cohorts choose to allocate liquid capital toward immediate travel, wellness, and self-actualization milestones rather than hording capital exclusively for traditional, late-stage old-age security. They seek a balanced life distribution model rather than delayed gratification.

Conclusion: Navigating the New Architecture of Longevity

While previous generations adhered strictly to a rigid, conventional work-retirement matrix centered around institutional dependency and static savings instruments, Millennials and Gen Z are deliberately architecting an entirely new paradigm. Their core emphasis on operational flexibility, values-driven corporate alignment, and digital financial fluency—accelerated by a hyper-scaling gig economy—proves that retirement planning in India has transformed from an isolated late-career corporate box check into an active, everyday wellness lifestyle strategy.

For forward-thinking organizations, financial institutions, and policy architecture leads, adapting to these evolving retirement trends is a critical priority. To successfully retain premium talent and foster true financial security across India’s modern workforce, the industrial ecosystem must reject legacy assumptions and design modular, accessible, and high-transparency financial solutions that match the fluid expectations of our future economy.