Introduction: Prioritizing your retirement planning at 50 without a robust nest egg can bring on a distinct sense of financial vertigo in a rapidly evolving Indian economy. Between escalating lifestyle costs, healthcare inflation hovering at 10-12%, and the stark absence of a universal social security umbrella, the realization that “time is running out” feels deeply urgent. Yet, starting your retirement planning at 50 isn’t a signal to panic—it’s your cue to pivot with aggressive, systematic clarity. Achieving a financial corpus of Min ₹4 Crores before you step away from your active career is completely realistic. By harnessing your peak earning years, practicing absolute financial discipline, and utilizing tactical equity mutual fund strategies during market corrections, you can bridge a twenty-year gap in just one decade.

1. Demystifying the Goal: Why Strategic Retirement Planning at 50 is Critical

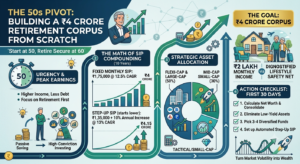

In India today, a retirement corpus is no longer just about survival; it is about maintaining your purchasing power against a stealthy thief called inflation. A corpus of ₹4 Crores, generating a conservative, inflation-adjusted post-tax return of 6% via systematic withdrawal plans (SWPs) and safe debt instruments, yields an annual income of approximately ₹24 Lakhs (or ₹2 Lakhs per month). This provides a resilient, dignified lifestyle safety net in any major Indian tier-1 or tier-2 city.

The perceived difficulty of building this corpus stems from traditional, risk-averse mindsets that default to Fixed Deposits (FDs) or Public Provident Funds (PPF). While safe, these instruments barely beat inflation. When you restructure your retirement planning at 50, you are likely at the absolute peak of your earning capacity. Corporate bonuses, high disposable income as children graduate, and settled home equity mean you can invest amounts that were unthinkable in your 20s or 30s. You can utilize structured tools verified by the Association of Mutual Funds in India (AMFI) to track baseline fund metrics. The path is not complex; it simply requires a shift from passive saving to high-conviction, structured investing.

2. The Math of Compounding: Setting Up the SIP Framework

To accumulate ₹4 Crores in a 10-year horizon (assuming retirement at age 60), we rely on systematic equity investments. Over a decade-long block, Indian equity mutual funds historically deliver an annualized return (CAGR) of 12% to 15%. Let’s look at how the math plays out under a standard model and an aggressive step-up approach:

| Investment Strategy | Monthly SIP Amount | Assumed Rate of Return (CAGR) | Total Tenure | Estimated Final Corpus |

|---|---|---|---|---|

| Fixed Monthly SIP | ₹1,75,000 | 12.5% | 10 Years | ~₹4.02 Crores |

| 10% Step-Up SIP (Starts lower) | ₹1,35,000 | 13.0% | 10 Years | ~₹4.15 Crores |

The Power of the Step-Up: Commencing with SIPinitial = ₹1,35,000 and increasing your investment amount by just 10% every single year aligns perfectly with annual salary increments and professional growth. This sharply lowers the initial monthly barrier, making the target highly accessible from day one.

3. Embracing Market Volatility: The Secret Weapon When Retirement Planning at 50

Most conventional financial advice suggests dialing down equity exposure as you get closer to retirement. However, when execution of your retirement planning at 50 starts late, market volatility is not your enemy; it is your single greatest wealth multiplier. When the Nifty 50 or Sensex experiences short-term corrections due to global macroeconomic factors, corporate earnings cycles, or geopolitical tensions, mutual fund Net Asset Values (NAVs) drop. This allows your regular monthly SIPs to accumulate substantially more units through Rupee Cost Averaging.

To accelerate your timeline toward the ₹4 Crore target, you must be prepared to go highly aggressive. This means allocating surplus funds, annual performance bonuses, or matured low-yield insurance policies directly into equity mutual funds during market dips. When the broader index panics, you buy more units. You can monitor direct market valuations on the official National Stock Exchange of India (NSE) platform. Over a 5-to-10-year holding period, these low-NAV units compound exceptionally fast, giving your portfolio the powerful upward trajectory needed to hit your targets early.

4. The Discipline Code: Peak Earnings and Tactical Cost Cutting

Building a multi-crore portfolio in a decade demands unconditional behavioral discipline. This isn’t about painful deprivation; it is about optimization during your highest-earning years. Consider this your “financial sprint.”

The Rules of the Financial Sprint:

- Automate the Aggression: Schedule your mutual fund SIPs for the 1st to 5th of every month, directly following your salary credit. You invest first, and live on what remains.

- Aggressive Lifestyle Monetization: Avoid upgrading cars, purchasing luxury lifestyle properties, or taking on high-interest consumer debt in your 50s. Redirect these potential outflows directly to your retirement fund.

- Repurpose Inefficient Assets: Liquidate old traditional insurance plans (such as low-yielding endowment policies) or stagnant real estate plots that yield less than 4-5% annually, and deploy that capital directly into dynamic equity funds.

5. Strategic Asset Allocation for Late-Stage Accelerators

To safely and reliably hit your Min ₹4 Crores milestone, your allocation strategy should focus primarily on growth assets, while maintaining a smooth transition plan as retirement approaches:

- Flexi-Cap & Large-Cap Funds (50%): Provides a stable bedrock of India’s top 100 blue-chip corporate leaders, offering consistent growth with lower downside risk during volatile periods.

- Mid-Cap & Broad Market Funds (30%): Captures the high-growth trajectory of India’s mid-sized enterprises, driving strong alpha generation over your 10-year timeline.

- Sectoral/Contra Funds & Small-Cap (20%): Highly tactical exposure to capture deep value during severe market corrections, providing the extra boost needed to exceed your target corpus.

6. Conclusion: Action Checklist for Retirement Planning at 50

Your journey to a ₹4 Crore retirement starts not with a major life overhaul, but with an immediate, deliberate shift in your financial habits. Within the next 30 days:

- Calculate your precise current net worth and consolidate any scattered small savings accounts.

- Eliminate low-yield assets like fixed deposits or traditional insurance policies that return less than 5%.

- Pick 3 to 4 high-conviction diversified equity mutual funds across Flexi-cap and Mid-cap categories.

- Set up an automated monthly step-up SIP to lock in your savings rate before discretionary spending occurs.

- Turn today’s market volatility into your personal wealth launchpad, and take full control of your financial future.