When planning for your golden years, traditional mindsets often steer you toward safety. Many Indian savers view the stock market with caution, focusing heavily on short-term market corrections rather than compounding growth. However, if your goal is building a robust retirement corpus that survives hyper-inflation and ensures lifelong financial independence, keeping equities out of your asset allocation is a systemic risk you cannot afford to take.

Historically, domestic equity markets have acted as the most dependable wealth-creation engines available, turning disciplined, consistent savings into sustainable retirement nest eggs. This comprehensive guide breaks down why equities are mandatory for multi-decade financial survival, how India’s premier indices reward patience, and how to construct a resilient asset allocation model.

Inside This Guide

Why Equities Are Mandatory for Retirement

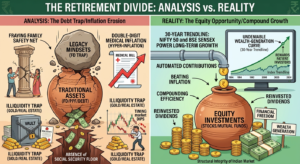

Inflation acts as a silent, continuous tax on your hard-earned savings. If your retirement portfolio consists solely of legacy fixed-income instruments like traditional fixed deposits (FDs), post office schemes, or low-yield bonds, your purchasing power will drastically decay over a multi-decade horizon.

Consider this: lifestyle and medical inflation across urban India frequently hits double digits. When your post-tax returns on debt instruments hover around 5–6%, a non-equity portfolio is effectively losing value every year.

Equities provide the heavy lifting required to outpace this purchasing power erosion. When you allocate capital to equity mutual funds or direct shares, you aren’t merely trading tickers or speculating on daily market movements. Instead, you are acquiring a direct ownership stake in the Indian corporate sector—the very engine driving the nation’s GDP growth. This long-term equity exposure ensures that your capital expands alongside the broader economy.

A Three-Decade Journey: The Power of Indian Indices

To grasp the compounding impact of long-term equity investing, one only needs to evaluate the historical performance of India’s benchmark indices: the BSE SENSEX and NIFTY 50.

Over the past 30 years, domestic indices have traversed major global crises, structural policy overhauls, geopolitical friction, and technological disruptions. Despite these sharp, short-term drawdowns, the structural trajectory of the Indian market has remained decisively upward, rewarding patient investors who looked past the noise.

As illustrated in our structural comparative infographic, trying to time these short-term market dips usually leads to underperformance. Investors who maintained disciplined, automated contributions (such as Systematic Investment Plans or SIPs) through economic troughs captured the most significant gains during subsequent recovery phases. Over a 30-year horizon, the volatility that terrifies short-term traders flattens out into an undeniable wealth-generation curve.

Core Reasons to Include Equities in Your Asset Allocation

A secure retirement strategy cannot rely on single-asset obsession. Equities deserve a permanent, foundational seat at your financial table for these primary reasons:

- Beating Structural Inflation: Over extended timelines, diversified equity portfolios are among the rare asset classes that consistently outpace retail and medical inflation, protecting your future purchasing power.

- The Velocity of Compounding: By staying invested and automatically reinvesting dividends, your corpus benefits from exponential compounding, where your accumulated gains begin generating wealth of their own.

- Extreme Tax Efficiency (The “No-Sell” Advantage): Unlike fixed deposits or regular bonds where interest is taxed annually, equities offer unmatched tax deferral. You do not incur any capital gains tax for 10, 20, or even 30 years—as long as you do not sell your shares. Your wealth grows completely unhindered by the taxman during your entire accumulation phase.

- Corporate Actions and Wealth Multipliers: Holding high-quality equities over decades rewards investors far beyond mere stock price appreciation. Long-term shareholders benefit from continuous corporate actions that multiply wealth, including:

- Regular Dividends: Providing a steady stream of passive income during your retirement years without eroding your core capital.

- Bonus Shares & Rights Issues: Rewarding loyal investors by multiplying your total share count over time without requiring extra capital outlays.

- Value-Unlocking Demergers: Major corporate restructurings—such as the spin-offs of Jio Financial Services from Reliance, ITC Hotels from ITC, or historical restructurings in FMCG majors like HUL—frequently unlock immense hidden value by handing shareholders free shares in newly listed, high-growth entities.

- High Liquidity and Transparency: Unlike illiquid physical assets like real estate or gold, which suffer from high transaction costs and transparency issues, equity markets offer clean, regulated liquidity. You can comfortably access or rebalance your capital exactly when needed.

Building Your Strategy: The Balanced Lifecycle Framework

An effective retirement blueprint uses equities as a primary growth driver while utilizing high-quality fixed income to provide immediate stability.

| Strategy Phase | Target Age Group | Recommended Asset Allocation Baseline |

|---|---|---|

| Accumulation Phase | Ages 25–45 | 70% to 80% Equities / 20% to 30% Fixed Income & Debt |

| Transition Phase | Ages 46–55 | 50% to 60% Equities / 40% to 50% Fixed Income & Debt |

| Preservation Phase | Ages 56+ | 30% to 40% Equities / 60% to 70% Fixed Income & Debt |

In your early and mid-working years, deploying a higher equity allocation allows your portfolio to comfortably absorb short-term volatility in exchange for maximizing long-term returns. As you draw closer to your target retirement age, you should gradually rebalance toward capital preservation assets.

However, your equity exposure should never drop to zero. Retaining a core 30% to 40% equity component during your actual post-retirement years ensures your nest egg continues to grow, protecting your corpus from running out during a retirement that could easily last 25 to 30 years.

The Bottom Line

Do not allow short-term market noise or legacy financial mindsets to compromise your financial freedom. By embracing the proven, transparent wealth-creation power of equities within a disciplined asset allocation framework, you can ensure that your retirement is not just stable, but prosperous.

Related articles

Young and planning retirement, know about Asset Allocation

Positive, practical retirement plan in your 50s