Published by: Kartikey Gupta

Optimizing your retirement asset allocation in your 30s is a crucial financial step to secure your long-term independence. Broadly defined, asset allocation is the process of spreading your investments across various asset classes such as equities, debt, gold, and real estate. This systematic approach balances risk and reward according to your personal financial goals, time horizon, and risk tolerance. For young professionals in India, choosing the right retirement asset allocation lays a solid foundation for wealth creation, harnessing the compounding power of investments while protecting your principal from sudden market fluctuations. In this article, we’ll explore the best avenues available and look at a balanced template to help you transition confidently into structured financial planning.

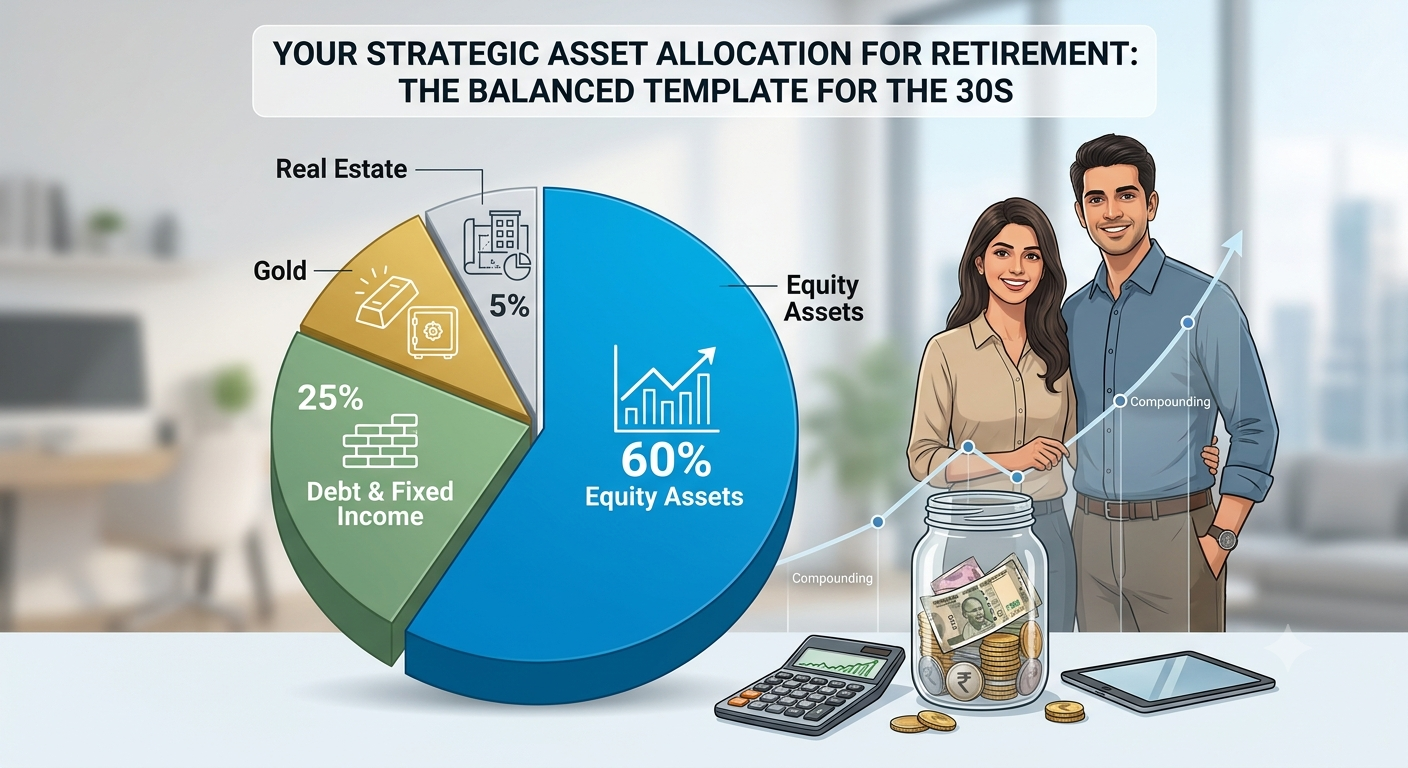

1. Balanced Retirement Asset Allocation for Your 30s

Your ideal strategic portfolio splits depend heavily on your distinct risk appetite, liabilities, and income stability. However, for a professional with a 25 to 30-year runway ahead, a growth-oriented retirement asset allocation serves as the most efficient defense against long-term inflation cycles.

| Asset Class | Target Percentage | Strategic Role & Common Instruments |

|---|---|---|

| Equity Assets | 60% | Primary engine for capital appreciation. Includes equity mutual funds, index funds, and ETFs. |

| Debt & Fixed Income | 25% | Capital preservation and interest accumulation. Covered via PPF, EPF, and fixed deposits. |

| Gold | 10% | Macroeconomic hedge and systemic fallback. Managed via Sovereign Gold Bonds (SGBs). |

| Real Estate | 5% | Liquid commercial real estate exposure without massive upfront overheads via REITs. |

Note: If your risk profile is conservative, increase your fixed income/debt allocation. For highly aggressive wealth builders, equity elements can easily scale higher.

2. Choosing Your Asset Allocation Mutual Funds & Instruments

Executing a reliable retirement asset allocation requires mapping allocations across highly transparent, institutional tools readily available in the Indian investment landscape:

A. Equity Selections (For Long-Term Compounding)

- Index Funds (Low-Cost Passive Trackers): Mirrors foundational market indices cleanly.

- Nippon India Nifty 50 Index Fund

- UTI Nifty 50 Index Fund

- Flexi Cap Funds (Dynamic Multi-Cap Allocation): Allows seasoned fund managers to shift weight dynamically between large, mid, and small-cap stocks.

- Parag Parikh Flexi Cap Fund

- SBI Flexi Cap Fund

- Large Cap Funds: Blue-chip corporate anchors providing steady fundamental backing.

- Axis Bluechip Fund

- HDFC Top 100 Fund

- ELSS (Tax-Saving Under 80C): Equity growth paired with direct statutory tax deductions.

- Mirae Asset Tax Saver Fund

- Axis Long Term Equity Fund

B. Debt, Fixed Income, & Pension Anchors (For Portfolio Balance)

- Public Provident Fund (PPF) & Employee Provident Fund (EPF): Exceptional debt foundations delivering safe, government-backed, tax-free interest generation matching retirement horizons.

- Short Duration Debt Mutual Funds: Minimizes systemic interest-rate risks while boosting overall cash portfolio liquidity.

- HDFC Short Term Debt Fund

- ICICI Prudential Short Term Fund

- National Pension System (NPS): Structured pension accumulation mechanism featuring additional tax-deductible benefits under Section 80CCD(1B).

C. Gold & Alternatives (Inflation Defense)

- Sovereign Gold Bonds (SGBs): Safest paper-gold format issued by the RBI. Offers zero storage risks, tax-free capital gains on maturity, and fixed annual passive interest.

- Gold ETFs / Digital Gold: Fractional, liquid trading allocations managed seamlessly through any retail brokerage portal.

D. Real Estate (Fractional Wealth Engines)

- Real Estate Investment Trusts (REITs): High-grade commercial real estate trusts (such as Embassy Office Parks REIT or Mindspace Business Parks REIT) offering distribution yields without physical management issues.

3. Blueprint: Example Monthly SIP Investment Framework

To see how a retirement asset allocation maps to a practical monthly budget, let’s assume a baseline investment capacity of An even ₹30,000 per month:

| Instrument Type | Monthly SIP Value (₹) | Core Strategic Rationale |

|---|---|---|

| Equity Mutual Funds (Index / Flexi Cap) | ₹18,000 | Maximizes exposure to market indices to drive primary alpha expansion. |

| Debt Mutual Funds / PPF Allocation | ₹7,500 | Suppresses short-term portfolio volatility and preserves principal. |

| Gold Options (SGBs / Liquid ETFs) | ₹3,000 | Supplements the core strategy as a safe-haven asset class against systemic inflation. |

| National Pension System (NPS) | ₹1,500 | Reinforces automated savings patterns and captures retirement tax offsets. |

| Total Outlay | ₹30,000 | Scale these numbers up linearly as your cash flow expands. |

4. The Math of Compounding: Target Corpus Calculation

When drafting financial plans in your 30s, accounting for lifestyle and healthcare inflation is absolutely crucial. A target corpus that sounds massive today can diminish in actual purchasing power 25 years down the road. Let us map how a regular monthly SIP stacks up over a 25-year investment window, assuming a balanced, multi-asset portfolio yield of 10% CAGR:

- Targeting a ₹1 Crore Corpus: Requires a disciplined commitment of Directly ₹13,000/month for 25 consecutive years.

- Targeting a ₹2 Crore Corpus: Scaled up to a commitment of Directly ₹26,000/month over the same timeline.

Starting early drastically reduces the amount you must save out of your pocket, because compounding does the heavy lifting for you.

📌 Important Strategy Resources for Retirement:

Before buying arbitrary products, review our foundational guide on What are Mutual Funds for Retirement? to optimize your long-term selections. Additionally, remember that successful asset planning is driven by psychology; safeguard your corpus by recognizing the Common emotional mistakes to avoid with your Retirement fund.

5. Professional Portfolio Management Tips

- Embrace Structural Simplicity: Do not dilute your concentration across dozens of mirror funds. A clean pairing of one Nifty 50 Index fund alongside a solid Flexi Cap scheme is a great start.

- Maximize Tax Shelters Wisely: Use ELSS products strategically under section 80C to protect your capital gains and income allocations concurrently.

- Optimize Your PPF Timeline: Invest your lump sums into your PPF account between the 1st and 5th of April every financial year to gain compounding interest benefits for the full twelve months.

- Rebalance Annually without Fail: A runaway market can skew your retirement asset allocation (e.g., pulling equity from 60% up to 75%). Once a year, lock in profits from outperforming sectors and re-allocate them into lagging asset categories to manage risk.

- Automate Your SIP Steps Up: Ensure you increase your retirement SIP allocations by 5% to 10% every single year in line with salary or consultancy revenue expansions.

6. Ready to Begin? Your Step-by-Step Action Plan

- Establish Clean Digital Infrastructure: Open an institutional account with trusted modern investment platforms (e.g., Zerodha, Groww, Kuvera, or IndMoney).

- Set Your Target Baseline: Document your asset allocation percentages clearly inside your personal investment registry.

- Automate Your Freedom: Configure automated electronic mandates for your monthly SIPs immediately following your standard payout dates to remove human emotion from trading.

- Monitor Passively: Revisit your portfolio structure solely during notable lifecourse shifts (marriage, children, property purchases) while tuning out daily market noise.

The Bottom Line: Your Future Self is Counting on You

Your 30s represent the most pivotal financial turning point of your career. It is the exact decade where lifestyle inflation can silently siphon off your wealth, or where structured discipline can buy your future early independence. Adopting a strict, automated retirement asset allocation prevents you from guessing or reacting to short-term volatility. You aren’t gambling on tomorrow; you are engineering it. Start small, automate completely, diversify across classes, and let time run your wealth engines. Your future self will thank you.