Generating Sustainable Passive Income for the Modern Indian Retiree

Retirement in India is undergoing a massive cultural shift. Moving away from the traditional model of total dependence on the joint family, today’s pre-retirees are looking toward a future of “active aging” and financial autonomy. However, the transition from a structured professional life to a self-determined one often brings a cocktail of anxieties—ranging from the rising cost of healthcare to the fear of outliving one’s corpus. Happiness in this phase is the presence of a robust, diversified plan. Even if you are in your 50s, you are not late; you are at the peak of your tactical potential to build a fortress of security.

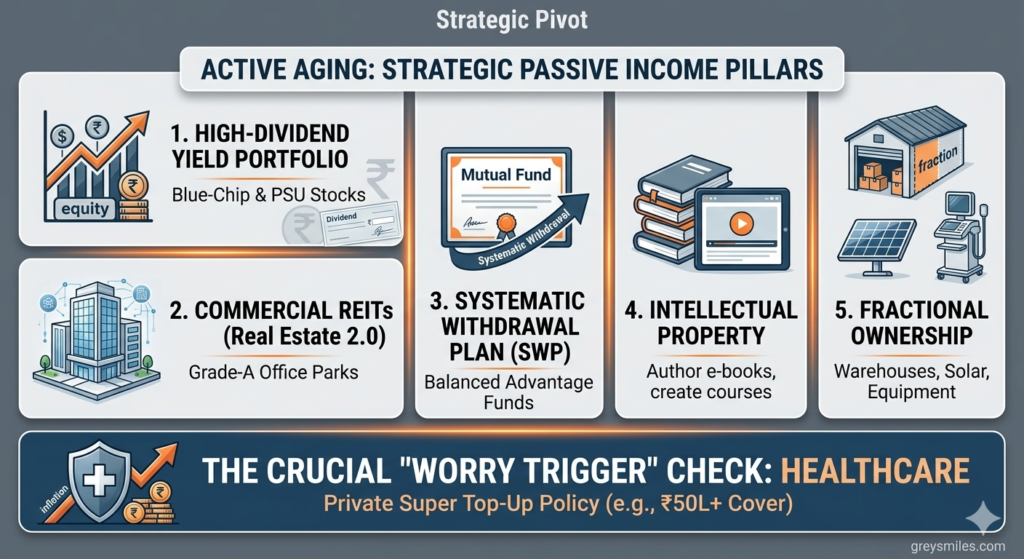

1. Dividend Strategy

2. Commercial REITs

3. Intellectual Assets

4. Systematic SWP

5. Health Resilience

1. High-Dividend Yield Portfolios (Equity)

In your 50s, the focus shifts from aggressive capital appreciation to consistent cash flow. Many Indian Blue-chip companies and Public Sector Undertakings (PSUs) offer yields that rival or beat traditional savings instruments.

- The Indian Context: Look for companies with a high “Dividend Payout Ratio.” While growth may be slower, the stability of quarterly or semi-annual payouts acts as a reliable secondary salary.

- Taxation Tip: Since dividends are now taxed at your income slab, they are most effective when your overall taxable income drops post-retirement.

2. Commercial Real Estate via REITs

Traditional property investment in India is often “land-rich but cash-poor.” REITs (Real Estate Investment Trusts) solve this by allowing you to invest in Grade-A commercial tech parks and office spaces with professional management.

| Asset Type | Entry Barrier | Liquidity | Payout Structure |

|---|---|---|---|

| Residential Flat | ₹75L – ₹2Cr+ | Very Low | Monthly (Inconsistent) |

| Listed REITs | ~₹50,000 | High (Stock Exchange) | Quarterly (Mandatory 90% Dist.) |

3. Content & Intellectual Property (IP)

Your 30+ years of professional wisdom is a high-value asset. Creating digital IP requires a time investment today for a perpetual return tomorrow.

4. Mutual Fund SWP (The “Synthetic” Salary)

Instead of high-risk P2P lending, many Indian retirees prefer a Systematic Withdrawal Plan (SWP) from a Hybrid or Balanced Advantage Fund. This creates a predictable monthly “salary” while keeping the core corpus invested in a mix of equity and debt.

- Tax Efficiency: Unlike interest or dividends, SWP withdrawals are treated as capital gains, which can significantly lower your tax liability compared to other fixed-income options.

5. The Healthcare Hedge

No income stream can survive the “worry trigger” of medical inflation, which in India currently hovers around 14%. To protect your autonomy, your healthcare plan must be independent of any previous corporate cover.

- Super Top-Up: A cost-effective way to push your coverage to ₹50 Lakhs or ₹1 Crore by keeping a high deductible.

- Preventive Asset: Investing in health check-ups and physical vitality in your 50s is the ultimate passive income—it prevents the massive “out-of-pocket” drains of your 70s.

Mathematical Sanity Check

To ensure your “music” never stops, account for the compounding effect of inflation. If your current monthly expenses are ₹1,00,000, at a 6% inflation rate, you will need approximately ₹3,20,000 per month in 20 years just to maintain the same standard of living.