Almost every modern retirement guide in India praises the Three-Bucket Strategy. The concept is elegant and intuitive: divide your retirement wealth into three distinct pools based on when you need the money, protecting yourself from market downturns while still beating inflation.

But while the theory is simple, the real-world execution trips up almost everyone.

“Once Bucket 1 runs out of cash, how exactly do I fill it back up? Do I sell my equities when the market is crashing? Do I shift money every year, or every three years? What about the taxes?”

If you don’t know the precise operational steps to rebalance your buckets, the strategy collapses into chaos. This guide provides the exact mechanical blueprint to route your money safely, manage market cycles, and optimize your taxes in retirement.

Quick Refresh: The 3-Bucket Architecture

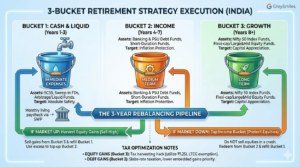

Before looking at the plumbing, let’s trace how a typical ₹2 Crore retirement portfolio is structured across the three buckets in the Indian context:

├── BUCKET 1: CASH (Years 1–3) -> Allocation: ~15% (₹30 Lakhs)

│ └── SCSS, Sweep-in FDs, Arbitrage / Liquid Mutual Funds├── BUCKET 2: INCOME (Years 4–7) -> Allocation: ~35% (₹70 Lakhs)

│ └── Banking & PSU Debt Funds, Corporate FDs, Short-Duration Funds└── BUCKET 3: GROWTH (Years 8+) -> Allocation: ~50% (₹100 Lakhs)

└── Nifty 50 Index Funds, Flexi-cap & Large-and-Mid Equity Funds

- Bucket 1 (Immediate – Years 1 to 3): Handles immediate monthly expenses. Stored in absolute safety: Senior Citizens Savings Scheme (SCSS), Arbitrage funds, and high-yield savings accounts.

- Bucket 2 (Medium Term – Years 4 to 7): Protects against near-term inflation. Stored in predictable, low-volatility debt assets: Banking & PSU Debt funds, Corporate Fixed Deposits, or short-duration funds.

- Bucket 3 (Long Term – Years 8+): Ensures your money doesn’t run out before you do. Stored entirely in Indian Equities (Index funds, Flexi-cap funds) to achieve long-term compounding.

The Core Problem: The 3-Year Depletion Mark

Imagine you start retirement on Day 1. Every single month, an automated Systematic Withdrawal Plan (SWP) or an SCSS quarterly payout routes money from Bucket 1 into your primary bank account.

Fast forward 36 months. Bucket 1 is now empty. Meanwhile, Bucket 3 (your equities) has been moving up and down with the stock market cycles. This is the exact moment where execution matters. You must execute a tactical rebalance to refill Bucket 1 without making emotional mistakes.

The 3-Year Rebalancing Blueprint: A Step-by-Step Sequence

To execute this properly, do not stress over your portfolio every single month. Set a calendar alert exactly every 3 years to run the following sequence:

1 | Assess the Health of Bucket 3 (Equities)Look at your equity bucket first. Has the Indian stock market been in a roaring bull run over the past 3 years, or is it currently sitting in a deep bear market or correction? Your next move depends entirely on this binary condition. |

2 | Scenario A: The Market is Up (Bull Run)If Bucket 3 has grown significantly (e.g., your initial ₹100 Lakhs grew to ₹140 Lakhs), harvest the profits directly from equities. Redeem ₹30 Lakhs worth of gains out of your equity funds. Move this cash directly into Bucket 1 to lock in another 3 years of stress-free living expenses. This is classic “selling high.” |

3 | Scenario B: The Market is Down (Bear Market)If the Nifty 50 has crashed or stagnated, do not touch your equities. Selling equities during a crash destroys long-term compounding. Instead, look at Bucket 2 (Fixed Income). Redeem ₹30 Lakhs from your low-volatility debt mutual funds or maturing fixed deposits, and move that into Bucket 1. This gives your equities another 3 years to fully recover. |

4 | Cascade Refilling (Only in Bull Markets)If it was a bumper bull market and you harvested significant equity gains in Step 2, use any excess profits beyond what Bucket 1 needed to top back up Bucket 2. This keeps your intermediate defensive safety net fully capitalized. |

The Tax Framework for Routing Money

Moving large sums between mutual funds in India triggers capital gains taxes. You must structure your exits cleanly to minimize what you owe the Income Tax Department.

1. The Equity Exit Route (Bucket 3 to Bucket 1)

When you redeem from Equity Mutual Funds during a bull run, you will trigger Long-Term Capital Gains (LTCG) tax if you held the units for more than 12 months.

- The Rule: Up to ₹1.25 Lakh per financial year of equity LTCG is entirely tax-free. Gains above this limit are taxed at 12.5%.

- The Execution Hack: Instead of withdrawing all ₹30 Lakhs on a single day at the 3-year mark, split the redemption across two financial years if possible (e.g., withdraw half in March and half in April) to utilize two separate ₹1.25 Lakh tax-free windows.

2. The Debt Exit Route (Bucket 2 to Bucket 1)

Following recent tax amendments, capital gains from Debt Mutual Funds are taxed strictly according to your regular income tax slab rate, regardless of how long you held them.

- The Execution Hack: Since debt redemptions add directly to your taxable income, prioritize withdrawing from schemes that have the lowest embedded gains first, or stagger the redemptions cleanly alongside your standard tax deductions (like Section 80D for senior health insurance premiums).

⚠️ The Golden Rule of Execution

Never automate the transfer from Bucket 3 to Bucket 1. Automated switches ignore market valuations. Rebalancing must remain a manual, deliberate decision made once every three years based purely on whether the equity markets are expensive or cheap.

Summary Checklist for Retirees

| Action Item | Frequency | Target Execution |

|---|---|---|

| Monthly Living Paycheck | Automated | Sent to your primary savings bank account from Bucket 1 via SWP. |

| Portfolio Performance Review | Annual | Ensure no single mutual fund is drastically underperforming its benchmark index. |

| The Great Rebalance Pipeline | Every 3 Years | Shift 3 years of expenses from Equity (if markets are up) or Debt (if markets are down) into Cash. |

By treating your retirement corpus as an interconnected pipeline rather than a static pool of money, you eliminate the fear of near-term market volatility and ensure a steady, un-disrupted paycheck throughout your golden years.

Also read: Why you should target 4 Crore retirement corpus?

Also read: 6 Stages of retirement planning