Planning for retirement in your 30s is a crucial financial step, and one of the most important aspects of this journey is how you allocate your investments—known as asset allocation. Asset allocation is the process of spreading your investments across various asset classes such as equities, debt, gold, and real estate. This approach helps balance risk and reward according to your financial goals, time horizon, and risk tolerance. For young professionals in India, the right asset allocation strategy lays a solid foundation for long-term wealth creation, harnessing the power of compounding while protecting against market fluctuations. In this article, we’ll explore the options available and a sample asset allocation to help you confidently plan your retirement.

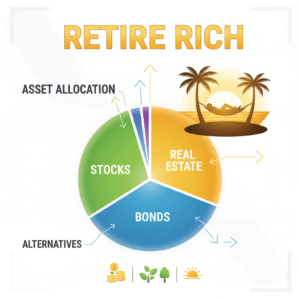

1. Sample Asset Allocation for Someone in Their 30s

Your allocation depends on your risk appetite, but here’s a typical moderate-risk example:

Asset Class | Percentage | Example Instruments |

Equity (Stocks/Mutual Funds) | 60% | Equity Mutual Funds, Index Funds, ETFs |

Debt/Fixed Income | 25% | PPF, EPF, Debt Mutual Funds, FDs, Bonds |

Gold | 10% | Sovereign Gold Bonds, Gold ETFs, Digital Gold |

Real Estate | 5% | Optional: REITs, Residential Plot, etc. |

Note: If you are conservative, increase debt/lower equity. For aggressive profiles, increase equity.

2. Example Mutual Funds (as of 2024)

A. Equity Mutual Funds (for long-term growth)

– Large Cap Fund:

– Axis Bluechip Fund

– HDFC Top 100 Fund

– Index Fund (low cost, passive):

– Nippon India Nifty 50 Index Fund

– UTI Nifty 50 Index Fund

– Flexi Cap Fund (multi-cap exposure):

– Parag Parikh Flexi Cap Fund

– SBI Flexi Cap Fund

– ELSS (Tax-saving under 80C):

– Mirae Asset Tax Saver Fund

– Axis Long Term Equity Fund

B. Debt Mutual Funds / Fixed Income

– Short Duration Debt Fund:

– HDFC Short Term Debt Fund

– ICICI Prudential Short Term Fund

– Bank Fixed Deposits (choose top private or PSU banks)

– PPF (offer best safety + tax-free interest, 15-year lock-in)

– EPF/NPS (for salaried/self-employed respectively)

C. Gold

– Sovereign Gold Bonds (SGBs by RBI, no making charges, 2.5% interest)

– Gold ETFs/Digital Gold through mutual fund platforms or brokers

D. Real Estate

– REITs (Embassy Office Parks REIT, Mindspace Business Parks REIT) for exposure without heavy capital

3. Example SIP Investment Plan

Assume you’re investing ₹30,000/month:

| Instrument | Amount (₹) | Rationale |

| Equity MF (Index/Flexi) | 18,000 | High long-term returns |

| Debt MF/PPF | 7,500 | Stability, safety, tax benefits (use PPF max if possible) |

| Gold (SGB/ETF) | 3,000 | Inflation hedge |

| NPS | 1,500 | Tax benefit + retirement corpus |

| Total | 30,000 |

Adjust as per your specific needs/goals/risk appetite.

4. Corpus Calculation Example

Suppose you want ₹1 crore (inflation-adjusted value) in 25 years:

– Monthly SIP needed (10% annual return) ≈ ₹13,000

– For ₹2 crore goal, about *₹26,000/month SIP* (using mutual fund calculators)

5. Pro Tips

– Start with Index/Flexi Cap funds if new to investing.

– Use ELSS funds for tax-saving under Section 80C.

– Max out PPF if you need safe, tax-free growth.

– Review your portfolio annually and rebalance if required.

– Increase your SIP as your income grows for superior compounding.

Also read: What are Mutual Funds for Retirement?

Common emotional mistakes to avoid with your Retirement fund

6. Action Steps

1. Open accounts with a reputed broker or mutual fund platform (like Groww, Kuvera, Zerodha, Paytm Money, IndMoney etc.).

2. Begin SIPs as per your asset allocation.

3. Automate investments and review once a year.

4. Track progress and make adjustments per life events (marriage, kids, home, etc.).

Disclaimer

– Past performance doesn’t guarantee future returns. Always review latest fund ratings and consult a certified financial advisor before taking decisions.

– Fund choices here are for illustration—do check current ratings, expense ratios, and latest performance.