Pillars of the FIRE Movement in India

Achieving early retirement requires a radical departure from mainstream consumer behavior. To successfully leverage the FIRE movement in India, practitioners rest their long-term financial architecture on three core strategic pillars:

- Aggressive Savings Rate: While traditional financial planning recommends saving 10% to 20% of income, FIRE followers systematically save 50% to 75% of their net take-home pay to maximize compounding potential early in life.

- Strategic, Low-Cost Investing: Rather than relying on traditional, low-yield vehicles like Fixed Deposits alone, practitioners favor index equity funds, direct equities, and tactical debt assets. You can design your long-term asset allocation framework by leveraging our Complete Strategic Guide to Mutual Funds for Retirement.

- Mindful Frugality and Minimalism: This involves separating happiness from consumerism. It does not mean deprivation; instead, it prioritizes “value spending”—eliminating lifestyle creep to maximize the active investment pool.

Benefits of Early Financial Independence

The primary asset the global early retirement philosophy buys isn’t luxury goods; it is ultimate time autonomy.

- Reclaiming Time Sovereignty: True financial independence allows individuals to design their days free from economic coercion. Whether that means changing careers, pursuing creative arts, or traveling, work becomes entirely optional.

- Mitigating Corporate Burnout: The fast-paced corporate ecosystem often takes a heavy mental and physical toll. Following this alternative career lifestyle acts as an exit roadmap, offering a structural shield against toxic workplaces. For a deeper analysis on how younger professionals are rewriting these rules, explore our feature on Retirement Trends: How Millennials and GenZ View Career and Retirement Planning.

- Generational and Personal Flexibility: Reaching financial independence early provides the freedom to be present for critical family milestones, slow down during prime health years, and build non-monetized passion projects.

Challenges and Realities of the Indian Financial Ecosystem

Transitioning the Western-born retirement model into the macroeconomics of developing markets requires major local adjustments. Those tracking the FIRE movement in India face unique systemic hurdles:

1. High Structural Inflation

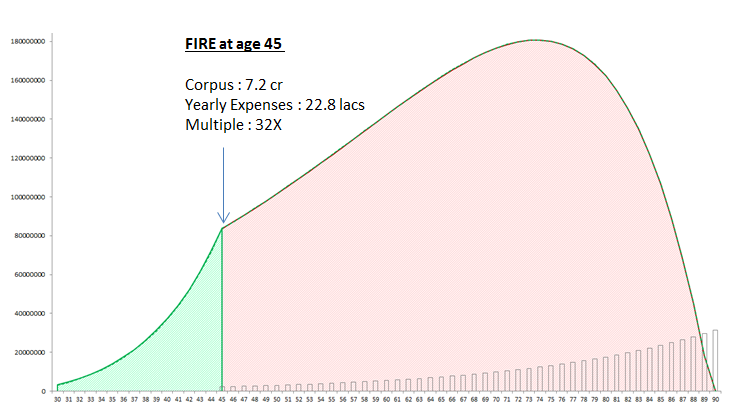

While Western models often calculate using a 2% to 3% long-term inflation rate, India’s historical consumer price index (CPI) hovering between 5% and 7% dramatically alters the mathematics. Lifestyle inflation—especially in tier-1 Indian cities—can be even higher. This requires a much larger “corpus multiple” (often 35x to 50x annual expenses instead of the standard Western 25x).

2. Market Volatility and Sequence of Returns Risk

The Indian equity market (represented by benchmarks like the NIFTY 50) offers strong long-term growth potential but is subject to emerging-market volatility. Experiencing a severe market downturn immediately after retiring—known as Sequence of Returns Risk (SRR)—can permanently damage a portfolio’s longevity if it isn’t properly diversified with debt instruments.

3. Limited Institutional Social Security

Unlike developed economies with robust social safety nets or state pension programs, retail investors in India bear 100% of their retirement, healthcare, and eldercare costs. According to data and research frameworks highlighted by institutions like the Indian Institute of Banking and Finance (IIBF), personal asset liability management is entirely self-directed.

4. Cultural and Multi-Generational Obligations

The Indian socio-economic fabric involves deep-seated familial financial interdependencies. A robust plan cannot look at individual expenses in isolation; it must explicitly account for supporting aging parents, sponsoring children’s escalating higher education costs, and contributing to family social milestones.

5. Hyper-Inflation in Healthcare

Medical inflation in India is rising at an estimated 10% to 14% annually. Without a corporate group health policy post-retirement, a single major medical emergency can wipe out an unprepared equity portfolio.

Variations of Retiring Early

Because a single financial blueprint does not fit everyone, the local community adopting the FIRE movement in India relies on several distinct variants of the core strategy:

| FIRE Flavor | Core Strategy | Ideal For |

|---|---|---|

| Lean FIRE | Extreme minimalism; maintaining a highly frugal lifestyle post-retirement on a lean corpus (20x to 25x base expenses). | Dedicated minimalists, singles, or those living in low-cost-of-living areas. |

| Fat FIRE | Accumulating a massive corpus (40x to 50x generous expenses) to enjoy an uncompromised, affluent lifestyle. | High earners who enjoy fine dining, luxury travel, and premium housing. |

| Barista FIRE | Quitting the corporate grind but keeping a low-stress part-time job or freelance gig to cover daily gaps without touching the core investment pool. | Individuals who want structural routine and active social engagement without corporate politics. |

| Coast FIRE | Front-loading investments aggressively in your 20s until the compounding math guarantees a comfortable traditional retirement, allowing you to spend 100% of your active income thereafter. | Young professionals who love working but want to stop stressing over long-term savings goals. |

Strategic Steps to Achieve Financial Independence

To successfully execute early retirement in India’s current financial climate, consider this step-by-step framework:

- Define Your Absolute FIRE Number: Calculate your current annual baseline expenses. Multiply this by an India-specific safety multiple to map your target milestones. For precise equations and adjustments, consult our full guide on How to Calculate Your Retirement Corpus in India.

- Optimize Asset Allocation: Build a diversified portfolio across Indian Equities (via low-cost index mutual funds for growth), Fixed Income (via the Voluntary Provident Fund (VPF), National Pension System (NPS), or debt mutual funds for stability), and Real Estate/Gold as alternative hedges.

- De-risk with De-coupling Insurance: Purchase private, super-top-up health insurance policies early while you are young and clear of pre-existing conditions. Pair this with a pure term life insurance policy that extends to your projected financial freedom age.

- Create a Dynamic Withdrawal Strategy: Instead of blindly relying on the Western “4% rule,” adopt a variable percentage withdrawal or bucket strategy. This keeps 3 years of living expenses in highly liquid cash equivalents to insulate your equity holdings from market crashes.