While conversations around the gender pay gap have finally entered corporate boardrooms in India, a far more devastating financial crisis remains quietly ignored: the Gender Retirement Gap. Globally, women retire with significantly less wealth than men, but in the Indian socio-economic landscape, this disparity scales up exponentially. Driven by longer life expectancies, fragmented career trajectories, and systemic institutional designs, an urban Indian woman’s pension accumulation can lag behind her male peers by nearly 40%. Achieving true structural financial independence requires looking past basic monthly savings and addressing the hidden, gendered realities of long-term wealth compounding.

Why It Is Missed: Social Norms & Fragmented Incomes

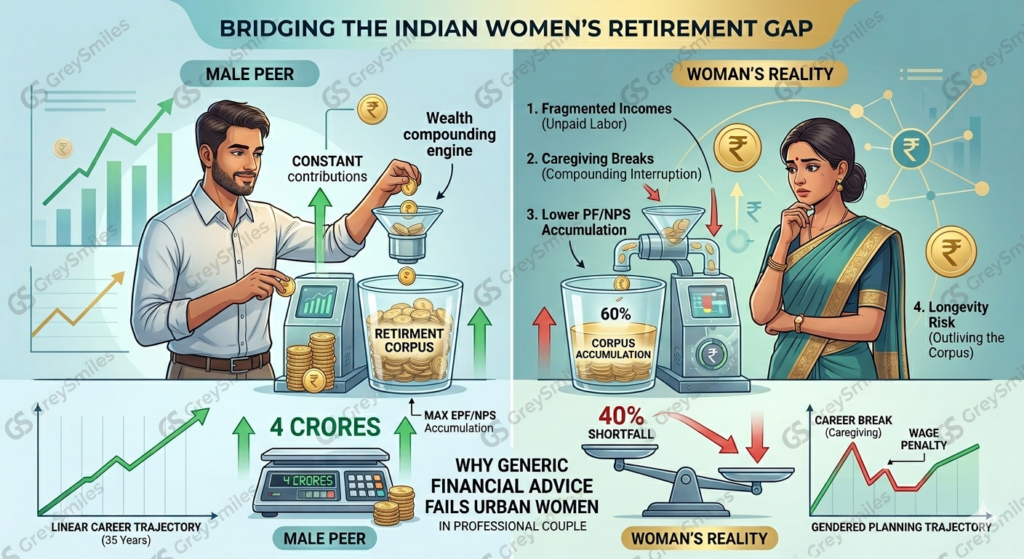

The core reason the retirement gap remains invisible is that conventional Indian financial planning assumes an unbroken, linear 35-year career graph. Societal expectations routinely disrupt this blueprint for women. Traditional norms position women as the primary, unpaid default providers for household management, childcare, and elder care.

This structural arrangement leads to deeply fragmented incomes. Even highly qualified corporate professionals often transition into lower-paying freelance roles, consulting, or part-time work to access flexibility. Because these income streams are irregular, active long-term retirement contributions get relegated to the background, masked behind the false security of a spouse’s primary corporate earnings.

The Multiplier Penalty: Caregiving Breaks & Compounding Interruption

In the math of wealth compounding, time matters more than the principal amount. When an employee takes a career break—whether for maternity, early childcare, or looking after aging parents-in-law—the damage to their retirement readiness extends far beyond the temporary loss of monthly income.

The Motherhood and Caregiver Penalty: Taking a modest 3-year sabbatical in your early 30s permanently alters your terminal wealth trajectory. It removes fresh contributions during prime earning years and flatlines the exponential growth phase of your existing money.

When re-entering the corporate workforce, women frequently face a “wage penalty,” restarting at lower compensation bands or missing key promotion cycles. This permanently lowers their lifetime earning capacity and restricts their ability to play financial catch-up in their 40s and 50s.

The Structural Shortfall: Lower EPF and NPS Accumulation

Statutory retirement instruments in India are inherently tied to formal, continuous payroll structures. When wages are lower or careers break, the long-term wealth anchors suffer immediate shortfalls:

- Employees’ Provident Fund (EPF): A 12% contribution matching structure means lower basic pay results directly in lower EPF accumulation. Resigning to take an extended break often leads to early EPF withdrawals to cover transitional phases, liquidating the retirement anchor completely.

- National Pension System (NPS): Corporate co-contributions under Section 80CCD(2) vanish entirely outside formal payrolls. Because retail individual accounts require active, disciplined execution, self-employed women or those on sabbaticals frequently experience lapse gaps in their NPS tier-1 architectures.

The Longevity Hazard: Survivor Benefits & Outliving the Corpus

The retirement math for Indian women must account for a harsh biological reality: Indian women, on average, outlive men by several years. Coupled with the common cultural practice of marrying older partners, a woman is highly likely to manage her retirement completely alone for the final decade of her life.

This reality introduces severe Sequence of Returns Risk and healthcare inflation shocks. Joint annuity payouts often drop significantly once the primary male account holder passes away, or traditional family assets get locked in complex probate processes. Lacking robust personal corpus allocations or clear survivor-benefit structures, older women face a steep risk of running completely out of money precisely when late-stage medical costs peak.

Correcting the Course: Targeted Financial Products for Women

Bridging this structural deficit requires moving beyond generic fixed deposits and adopting defensive tactical frameworks optimized for interrupted career timelines:

| Vehicle / Strategy | Indian Financial Context Implementation | Targeted Benefit for Women |

|---|---|---|

| Voluntary Provident Fund (VPF) | Voluntarily scaling personal EPF contributions up to 100% of basic pay during active employment. | Maximizes safe, tax-free compounding returns to act as a financial cushion before any intended career breaks. |

| Automated SIP Step-Ups | Utilizing Equity Mutual Funds with a mandatory 15% annual auto-escalation trigger. | Aggressively builds up principal equity during active earning years to offset future gaps. |

| Standalone Health Insurance | Buying a dedicated personal healthcare base plan + Super Top-Up separate from family/spouse corporate covers. | Guarantees continuous, uncompromised insurability throughout career breaks and through widowhood. |

| Active PPF Maintenance | Depositing a minimum of ₹500 annually in a personal Public Provident Fund during career breaks. | Prevents account deactivation, preserves the sovereign tax-free status, and secures long-term compounding. |

Real Proof: Strategic Frameworks in Action

This structural challenge can be navigated successfully with proactive positioning. Consider a case study of a 34-year-old product manager based in Bangalore who planned a 4-year transition out of corporate tech to raise her child and establish an independent consulting practice.

Instead of letting her retirement assets stagnate, she systematically restructured her portfolio:

- She optimized her active corporate payroll by maximizing her VPF allocation to lock in fixed income returns.

- Before exiting her corporate role, she established a private, high-sum-insured health insurance policy, neutralizing the risk of losing her corporate group cover.

- During her consulting transition, she maintained her personal NPS account manually via digital apps, ensuring her equity compounding engine never paused.

By treating her career break as a predictable, structured timeline rather than an unplanned financial pause, she protected her path toward her core retirement goal. Securing a comfortable long-term future demands changing the approach: treating women’s financial planning as a distinct, strategic blueprint that requires independent execution.

Related Articles:

Are women well prepared for retirement in India

Retirement Planning in India: How to Calculate Your Retirement Corpus for Couples vs Singles

Frequently Asked Questions

What is the gender retirement gap in India?

The gender retirement gap in India refers to the structural disparity where urban women accumulate up to 40% less retirement wealth than men. This gap is driven by lower average lifetime wages, multi-year caregiving career breaks, and systemic interruption of compounding vehicles like EPF and NPS.