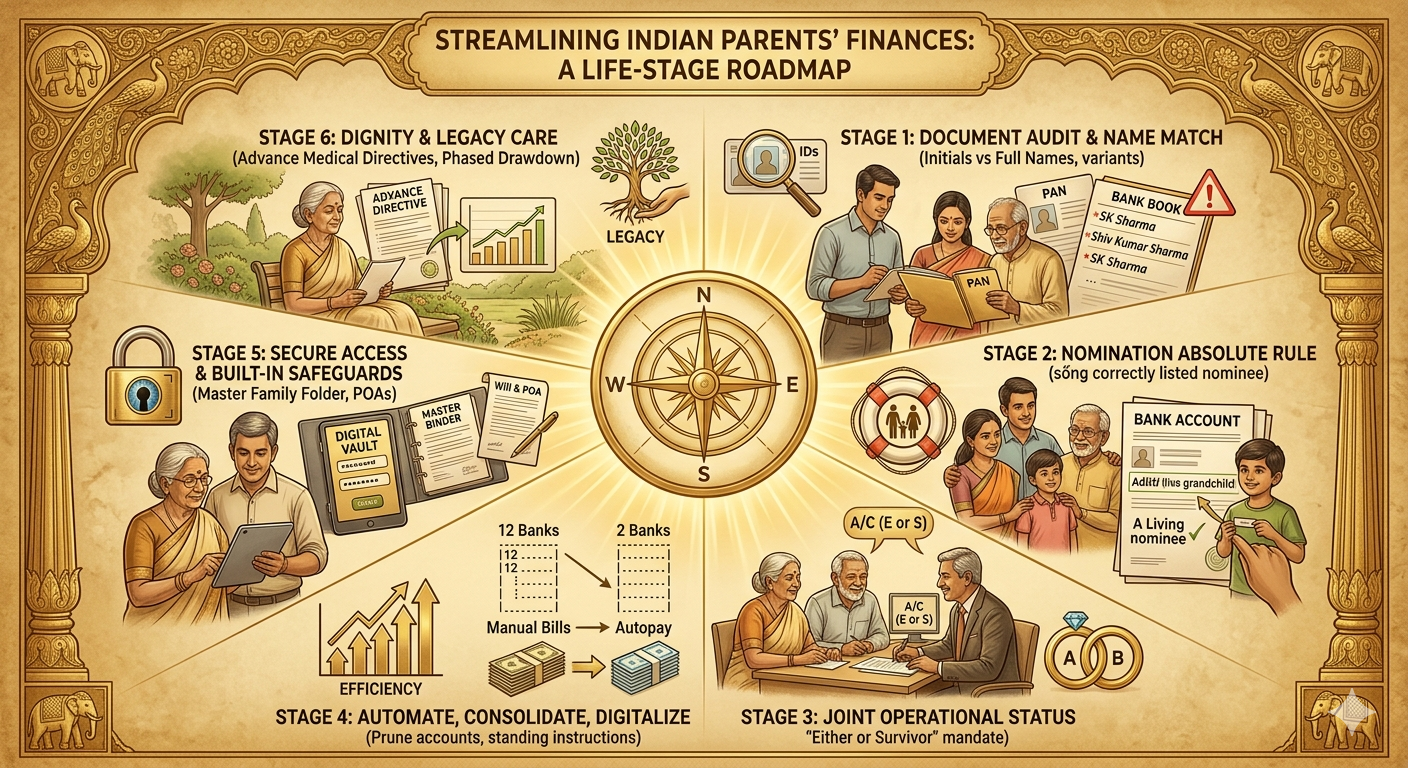

Helping our aging parents simplify their financial world is one of the most profound, practical acts of care we can offer. As they navigate their golden years, the transition from paper-based legacy systems to an increasingly digital banking ecosystem can become a source of immense friction rather than convenience. For those of us in our 40s or 50s, stepping in to help isn’t just about organizing dusty files—it’s about actively protecting their hard-earned legacy and ensuring their comfort.

In the Indian context, this process frequently hits a massive, bureaucratic roadblock: the dreaded name mismatch. Whether it is S.K. Sharma, S. Kumar Sharma, or Shiv Kumar Sharma, minor discrepancies across documents like bank accounts, insurance policies, and property titles can freeze accounts and cause massive structural headaches during critical healthcare claims or asset transmissions. This guide provides a battle-tested roadmap to secure your family’s financial peace of mind.

Quick Navigation Hub

Click any section below to jump directly to that phase of the guide:

Phase 1: The Document Audit & The Name Mismatch Fix

In India, names have historically been treated fluidly on paper, but modern financial institutions and centralized databases require absolute, character-for-character consistency. A single misplaced initial or an omitted middle name can freeze a senior citizen’s account or halt an estate transfer entirely.

1. Identify the Discrepancies

Gather your parents’ physical folders and perform a rigorous cross-match across their entire document ecosystem. Look closely for these common variations:

- Initials vs. Full Names: Expansions or contractions of middle names and last names (e.g., V.P. Singh vs. Vijay Pal Singh).

- Dropped Elements: Omission of regional, ancestral, or community sub-castes in newer digital IDs compared to old bank books.

- Spousal & Surname Shifts: Legacy insurance policies still carrying a mother’s maiden name rather than her married name.

- Transliteration Errors: Variations caused by translating regional scripts into English records over decades (e.g., Banerjee vs. Bandopadhyay, or Desai vs. Desae).

2. Standardize and Execute the Correction Roadmap

Do not wait for an emergency or a medical crisis to discover an error. Execute these proactive corrections immediately:

- Establish the “Anchor Identity”: Choose one definitive, official spelling to act as the legal baseline—typically the spelling that aligns with their current PAN card and core government identity databases.

- Update KYC Proactively: Visit the primary bank branches, insurance providers, and mutual fund registrar offices (like CAMS or KFintech) to align historical records with the chosen anchor identity.

- Execute a “One and the Same” Affidavit: For older property deeds, physical share certificates, or legacy investments where altering the original document is functionally impossible, have your parents sign a “One and the Same Person” affidavit before a registered notary. For severe discrepancies, look into a formal Gazette Notification.

- Synchronize Tax Registries: Verify that their PAN and core government identity details are fully linked and matching perfectly. Minor mismatches here can prevent successful tax filings or cause sudden automated compliance freezes.

- Maintain a Digital “Alias Master Folder”: Create a secure spreadsheet detailing every historical name variation, backed up by scanned copies of legacy passports, school leaving certificates, or old utility bills that link those identities together.

Phase 2: Structural Verification (Ownership & Nominations)

An asset is only secure if it is structured to transition seamlessly to the next generation. Missing, incomplete, or outdated structural details are the single greatest cause of billions of rupees sitting as unclaimed wealth across Indian financial institutions.

1. Enforce the “Nomination Absolute” Rule

Check every single active bank account, fixed deposit, post office savings scheme, mutual fund folio, demat account, and safe deposit locker. Ensure that a living, legally identifiable nominee is explicitly registered. Ensure that the nominee’s name is written exactly as it appears on their official government ID cards to prevent future estate transmission hurdles.

2. Transition to Joint Operational Status

Whenever practical, convert single-holder operational bank accounts into joint accounts featuring an “Either or Survivor” operating mandate. This can be done with a spouse or a trusted adult child, ensuring that funds remain immediately accessible for daily household needs or medical requirements if one holder becomes incapacitated. Similarly, review physical property deeds to clarify survivorship pathways.

Phase 3: Automate, Consolidate, and Digitalize

A fragmented portfolio is inherently vulnerable. Consolidating assets dramatically reduces cognitive fatigue for aging parents, limits administrative maintenance, and makes comprehensive portfolio oversight a breeze.

| The Fragmented Baseline (Old Way) | The Streamlined Standard (Modern Way) |

|---|---|

| 10+ scattered bank accounts across cities. | 2 centralized banking relationships. |

| Physical utility bills tracked via paper mail. | Automated Autopay & standing instructions. |

| Scattered physical certificates and lost slips. | Unified Demat account & encrypted digital vaults. |

1. Aggressive Account Consolidation

- Prune Dormant Accounts: If your parents have accumulated multiple accounts from past employers or old neighborhood branches, close them down. Consolidate their liquid net worth into two primary banks: one top-tier bank for operational cash flow, and one secure institution for long-term safe deposits.

- Unify Mutual Fund Portfolios: Migrate scattered mutual fund holdings into a single demat account or use unified platforms to track overall asset allocation under one clear dashboard.

2. Establish Automated Cash Workflows

Set up robust Standing Instructions (SI) or net-banking Autopay for all recurring essentials: electricity bills, piped gas, society maintenance charges, and—most importantly—health insurance premiums. Missing a premium payment due to forgetfulness can cause a catastrophic lapse in critical insurance coverage when it is needed most. Transition accounts to paperless e-billing, and route those alerts into a shared family email inbox.

Phase 4: Secure Access and Built-in Safeguards

Organization is only effective if the right people can securely access the system during an emergency. Your objective is to build a highly secure, reliable operational bridge between your parents’ legal records and your supervisor oversight.

1. Architect the Master Family Folder

Build a comprehensive, two-part record keeping system:

- The Digital Vault: Utilize a reputable, encrypted password manager or a highly secure cloud folder to archive banking customer IDs, online net-banking credentials, and account numbers. Never share unencrypted passwords or financial credentials over standard mobile chat applications.

- The Physical Binder: Maintain a well-indexed, fireproof physical binder containing original Wills, real estate deeds, physical share certificates, and current health insurance cards.

2. Secure Clear Legal Agency

Ensure your parents have updated, legally unambiguous **Wills** drafted and signed by witnesses. Furthermore, discuss and put in place a Durable Power of Attorney (POA) and an Advance Medical Directive (Living Will) while they are in full health. This grants you clear, legal authorization to step in and manage essential medical and financial choices if they ever face temporary cognitive or physical incapacitation.

3. Deploy Proactive Digital Guardrails

Verify that real-time SMS and email transactional alerts are active on your parents’ primary phones so you can instantly spot unusual activity. Maintain a separate emergency cash reserve in a highly liquid asset class (like a premium liquid fund or high-yield savings account) that you can tap into immediately during an unannounced medical emergency.

Over to You

Navigating the administrative rules of Indian financial systems while balancing family dynamics takes immense care and patience, but it is an invaluable gift. If you have already helped your parents correct name discrepancies, transition old physical shares, or build a clean estate plan, what hurdles did you encounter? What strategies worked best for your family? Share your insights in the comments below!

Related Articles:

Myths around Nominee, Joint applicant and a Will

The Unclaimed Wealth Crisis in India Why Crores Remain Untransferred to Rightful Heirs