Mastering budgeting for retirement has transformed from a distant lifestyle choice into an immediate survival strategy for India’s younger workforce. In a world where economic self-reliance is increasingly prized, young adults face an unprecedented financial landscape marked by shifting macroeconomic currents, steep real estate premiums, and core structural inflation. Millennials and Gen Z are encountering vastly different economic realities than previous generations, who often relied on linear career paths, fixed corporate benefits, and static pension anchors. Data from global studies, including the Employee Benefit Research Institute , reveals a glaring generational anxiety: nearly 60% of Millennials and 70% of Gen Z express deep concern that their current savings trajectory will not sustain their post-employment years. However, by deploying structured capital allocation techniques early, you can systematically convert your active monthly cash flow into a resilient, long-term compounding machine.

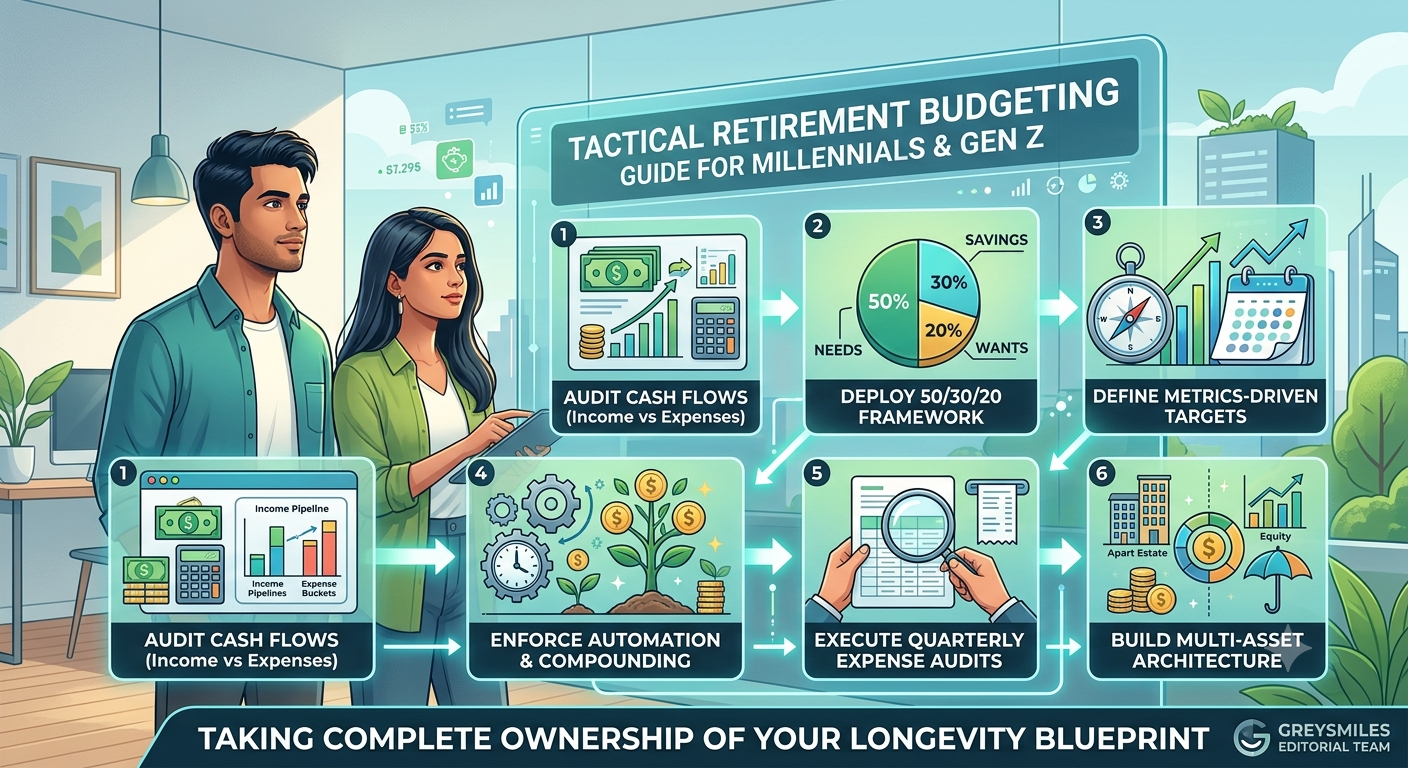

Quick Navigation Links Step 1: Audit Your Cash Flows (Income vs. Expenses) Before executing any long-term plan, you must gain absolute visibility over your entire capital ecosystem. When it comes to budgeting for retirement , digital natives navigating a fragmented, multi-client gig economy face the unique challenge of aggregating multiple fluid pipelines rather than relying on a single monthly payslip.

Consolidate Inflow Channels: Systematically log all distinct revenue paths, including your primary corporate salary, cross-border freelance invoices, digital consulting retainers, and secondary side hustle payouts.Segment Fixed vs. Variable Outflows: Clearly separate absolute monthly contractual obligations (rent, home loan EMIs, utilities, software subscriptions) from highly dynamic variable outflows (dining out, lifestyle spending, leisure travel).Data from the Reserve Bank of India banking data indicators highlights a critical baseline behavior: approximately 55% of Indian Millennials allocate over 30% of their net take-home pay to purely discretionary, variable expenses. This widespread structural leak underscores the vital necessity of tracking your baseline spending patterns before allocating investment surpluses.

If you are looking for immediate freelance avenues to scale up your primary cash inflow, explore our comprehensive tracking guide on Side Hustles and Retirement Planning Options in India .

Step 2: Deploy the 50/30/20 Budgeting for Retirement Framework To shield your wealth accumulation strategy from emotional or reactive spending, map your aggregate monthly income into a clean, systematic allocation framework. A highly resilient architecture for early-stage wealth building is the classic 50/30/20 ruleset:

Allocation Percentage Core Category Focus Operational Elements Included 50% Needs (Absolute Essentials) Housing rent/EMIs, baseline groceries, essential healthcare premiums, transport, and basic utilities. 30% Wants (Discretionary Lifestyle) Premium dining out, streaming entertainment, travel, and non-essential luxury shopping. 20% Savings (Future Capital Preservation) Emergency liquid runways, National Pension System (NPS), and equity mutual fund SIPs.

Despite the simple math behind this breakdown, implementing it remains an exceptionally rare practice. Metrics from regional fintech audits indicate that a mere 30% of Millennials actively track their day-to-day capital expenditure. Without establishing this diagnostic habit, your critical 20% savings bucket is routinely consumed by gradual lifestyle creep.

Step 3: Define Metrics-Driven Retirement Targets Vague saving goals yield inconsistent investment discipline. Strategic budgeting for retirement requires calculating exact mathematical targets aligned directly to inflation-adjusted projections.

Project Future Income Multipliers: Macro indexes confirm that the vast majority of young Indian professionals expect to require 70% to 80% of their peak pre-retirement income to maintain structural lifestyle parity in their post-employment years.Deploy Mathematical Rules of Thumb: Utilize automated financial calculation engines to establish your terminal corpus target. A standard target baseline is to accumulate roughly 10 to 12 times your final annual salary, safely insulated within dedicated compounding channels, by the time you choose to step away from full-time corporate roles.For a complete, deep-dive breakdown on aligning your targets to specific asset instruments, review our Complete Guide on Mutual Funds for Retirement Corpus Building .

Step 4: Enforce Automation & Compounding Velocity Human willpower is an unreliable financial mechanism when pitted against immediate consumer temptations. The optimal method for protecting your future wealth from impulse spending is to completely remove human intervention from your routine.

Configure automated standing instructions and Systematic Investment Plans (SIPs) to execute precisely 24 to 48 hours after your primary paycheck hits your account. By treating your retirement allocation as a non-negotiable fixed debit, you adapt to live entirely on the residual cash flow. Furthermore, scaling your retirement contributions by a mere 1% sequentially each year dramatically compounds your terminal corpus over a multi-decade horizon due to the mathematical effects of geometric compounding.

Step 5: Execute Quarterly Expense Audits A sustainable budget is an evolving lifestyle blueprint, not a static, punishing document. As your career transitions through salary increments, unexpected freelance bonuses, or major lifestyle shifts, your tracking framework must adjust accordingly.

Leverage mobile financial logging applications or localized digital ledger tools to track your micro-transactions in real time. Quantitative industry data indicates that 30% of young Indians consistently overspend their pre-planned budgets on entertainment and premium dining. Identifying these behavioral anomalies early allows you to execute immediate micro-budget adjustments, systematically rerouting leaking capital back into long-term wealth preservation.

Step 6: Build a Multi-Asset Investment Architecture Accumulating capital inside a low-yield savings account guarantees purchasing power erosion via core inflation. A rigorous approach to budgeting for retirement requires routing your budgeted surplus across a highly diversified, tax-efficient market matrix.

Maximize Equity-Driven Velocity: Allocate a calculated percentage of your savings toward diversified mutual funds, index funds, and equities. Because Millennials and Gen Z possess an extended multi-decade time runway, their portfolios can safely absorb short-term market volatility in exchange for historical long-term equity premiums.Anchor with Government-Backed Regulated Portals: Secure your portfolio’s base by consistently maximizing contributions to the National Pension System (NPS) and the Public Provident Fund (PPF). These institutional channels provide vital structural guardrails, offering specialized tax deductions under Section 80C and Section 80CCD of the Income Tax Department guidelines, while locking in capital compounding far away from daily spending temptations.Conclusion: Taking Complete Ownership of Your Longevity Blueprint For India’s modern Millennial and Gen Z workforce, mastering budgeting for retirement is far more than a routine monthly financial tracking exercise—it is an intentional act of deliberate self-direction. As traditional corporate pensions fade and macroeconomic variables scale, building an automated, multi-asset financial architecture is the only definitive method to secure your long-term independence.

By auditing your cash flows today, enforcing the 50/30/20 ruleset, and methodically scaling your contributions by even 1% annually, you fundamentally alter your lifelong wealth trajectory. Every minor allocation adjustment executed during your early career phases expands exponentially over time through the pure physics of compounding. Do not delay your financial insulation. Begin your journey toward absolute financial peace of mind today by prioritizing your future self.