Published by the Financial Wellness Editorial Team

The gig economy has witnessed significant growth in India, with millions of young professionals opting for freelance work and non-traditional employment arrangements. According to data tracking modern workforce shifts, nearly 25% of the Indian workforce was engaged in freelancing as of 2023, with projections suggesting the gig economy could account for up to 50% of India’s total workforce by 2025. While freelancing offers unparalleled flexibility and the opportunity to pursue varied professional interests, it also poses unique structural challenges when it comes to long-term financial stability.

Without the safety net of statutory corporate structures, execution of proactive retirement planning for freelancers in India has transformed from an optional milestones into a critical survival metric. For an independent workforce managing volatile cash flows, building a resilient, self-reliant financial cushion early is paramount to long-term peace of mind.

1. Understand the Importance of Retirement Planning

Unlike traditional employees, freelancers do not enjoy employer-sponsored retirement systems like corporate provident funds or gratuity structures. This complete lack of automated institutional benefits makes it even more crucial for freelancers to proactively plan and save for their future self. The earlier independent professionals start saving, the more effectively they can leverage the power of geometric compounding to grow their terminal retirement funds from a volatile income base.

2. Choose the Right Retirement Accounts

In India, freelancers and gig workers do not have access to mandatory corporate provident funds, but it is vital to ruthlessly maximize the voluntary savings architectures that do exist. Key pillars to evaluate include:

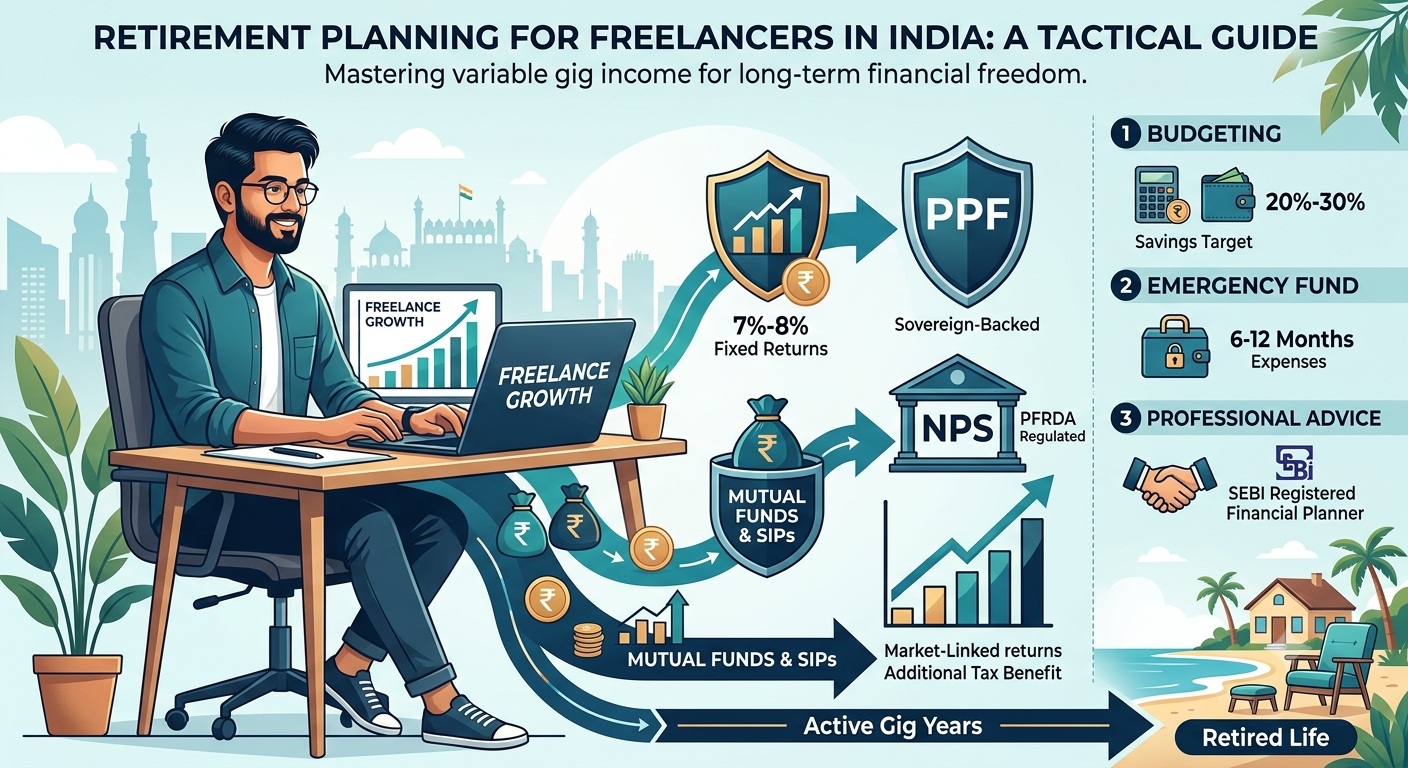

- Public Provident Fund (PPF): This sovereign, government-backed savings scheme offers highly reliable fixed interest rates (traditionally averaging around 7% to 8%) coupled with robust tax benefits under Section 80C of the Income Tax Act. The mandatory statutory lock-in period of 15 years acts as an excellent behavioral mechanism to encourage multi-decade, long-term saving. Official terms can be audited directly on the India Post National Savings Portal.

- National Pension System (NPS): Regulated by the PFRDA, the NPS is a voluntary, long-term pension architecture that allows independent earners to accumulate market-linked wealth. Contributions offer upfront tax deductions, and the framework allows you to actively tune a mix of Equity (E) and Debt (C and G) investments to match your precise risk profile. You can register an account online via the official Pension Fund Regulatory and Development Authority Portal.

- Mutual Funds and Systematic Investment Plans (SIPs): Freelancers can bypass lock-in constraints entirely by systematically routing capital into equity mutual funds to beat long-term inflation. Assessing your personal volatility tolerance remains an essential step before selecting specific aggressive or hybrid equity fund categories.

3. Budgeting for Retirement Contributions

Setting a realistic budget is crucial for effective retirement planning for freelancers in India. Independent professions naturally experience income fluctuations—often characterized by alternating “feast and famine” phases. This reality makes it essential to create a budget that accommodates both fixed living costs and variable savings thresholds.

A strong rule of thumb is to target saving at least 20% to 30% of your average gross monthly income exclusively toward retirement platforms.

While executing consistent monthly contributions may seem challenging during lean business cycles, creating an insulated cash buffer allows savers to smooth out these monthly capital variations without breaking their compounding trajectory.

4. Investing Wisely

As your independent enterprise grows and yields surplus cash flow, freelancers should purposefully diversify their investment portfolios far beyond low-yield traditional savings accounts to insulate their long-term purchasing power:

- Index Funds / ETFs: These low-cost passive instruments mirror broad stock market indices, allowing gig workers to gain broad equity exposure with reduced fund manager risk and minimal expense ratios.

- Real Estate: For high-earning freelancers, investing in tangible real estate assets can build a parallel secondary income engine through consistent rental yields, providing a reliable baseline cash flow during retirement phases.

5. Create an Emergency Fund

An emergency fund acts as an indispensable operational shock absorber for freelancers, given the inherent unpredictability of contract renewals and client payment timelines. Most seasoned financial advisors recommend maintaining a dedicated liquid fund holding **6 to 12 months’ worth of essential living expenses**. Having this pristine capital reserve explicitly prevents independent professionals from being forced to prematurely liquidate or draw down long-term retirement accounts during temporary macroeconomic downturns.

6. Utilize Technology for Financial Management

Modern fintech applications offer powerful tools to help independent contractors automate tracking and bypass administrative friction. Compliant platforms like Zerodha, Groww, or INDmoney assist savers in tracking asset allocation, monitoring investment progress, and auditing recurring expenses. Leveraging these tools simplifies wealth tracking and builds automated consistency, ensuring freelancers maintain disciplined savings habits without manual intervention.

7. Seek Professional Advice

Finally, consider collaborating with a SEBI-registered fee-only financial planner or specialized retirement planner who thoroughly understands the specific tax nuances, volatile income streams, and systemic cash flow challenges unique to the gig economy. A professional can help draft personalized strategies to optimize your annual tax liability under current provisions managed by the Income Tax Department of India.

Conclusion: Owning Your Independent Financial Future

As the gig economy continues its massive expansion across India, freelancers and non-traditional professionals must adopt an aggressive, proactive approach to building their retirement safety net. In the absolute absence of corporate-mandated security, the responsibility to cultivate robust financial habits and execute informed investment decisions falls squarely on the individual.

By combining fixed, sovereign-backed options like the Public Provident Fund with the high-velocity compounding power of equity markets and index funds today, independent workers can design a life that pairs modern professional liberty with unconditional future financial security. The math heavily favors those who take action early. Embrace the freedoms of the modern gig lifestyle, but safeguard your future peace of mind—your future self will thank you. To begin calibrating your specific parameters, access our interactive freelancer retirement compounding tool to calculate your projected target corpus.

Related articles:

Retirement Trends: How Millennials and Gen Z Are Shaping the Future of Work and Retirement

Retirement Trends: How Millennials and GenZ view career and retirement planning